| > The Appraiser Coach > AMC Guide > OREP E&O ★★★★★ |

2026 Appraiser Survey: State of the Profession

by Isaac Peck, Publisher

Nearly one-third of all practicing appraisers plan to leave the profession within three years. Add the next cohort and roughly half intend to exit within the next five years.

Those are the headline numbers from Working RE‘s 2026 State of the Profession Survey, completed by approximately 1,800 appraisers nationwide in early 2026.

Before the retirement cliff narrative takes hold, consider this: Working RE ran a nearly identical question in its 2016 Future of Appraising Survey. At that time, 33 percent of respondents planned to retire within five years, and more than half within 10 years. Today, a decade later, most of them are still appraising.

The pattern goes back further still. In a 2009 Working RE survey (18 years ago), conducted at the bottom of the financial crisis with over 6,200 respondents, over 53 percent of appraisers said they did not expect to be appraising full-time five years from then. While the profession did see some attrition over the next five years due to the incredibly slow market that followed the 2008 real estate crash, the fallout was nowhere close to 50 percent of the profession, or even 25 percent.

Appraisers consistently overpredict their own demise. Retirement intentions and actual retirements are different things, and appraisers have a long track record of staying longer than they expect. The profession accommodates part-time schedules, requires no storefront or staff, and provides income that many practitioners continue to rely on well into their 60s, 70s and 80s. However, whether the UAD 3.6 transition will finally accelerate actual exits in a way prior inflection points did not, remains to be seen.

Mark Twain wrote that “history doesn’t repeat itself, but it often rhymes.” In the years following the 2008 financial crisis, the market was slow and appraisers struggled with low volume and low fees. Fannie Mae and Freddie Mac (the GSEs) also pushed forward a huge data standardization project, UAD 2.6, which launched in 2011.

Similarly, today appraisers are facing low volume, fee pressure, and a transition to UAD 3.6 that is bringing anxiety and concerns. The demands of the new form are genuinely different from prior pressure points, and the combination of more work, an aging workforce, and a thin pipeline of new entrants arguably creates conditions that prior surveys did not fully capture.

Different This Time?

Working RE spoke with Jim Park, President of the Collateral Risk Network (CRN) and the former Executive Director of the Appraisal Subcommittee, to get his read on the survey findings. Park says the 2026 numbers reflect a genuine inflection point, not a repeat of the false alarms that preceded them.

“This time it’s different,” Park says. “We’ve reached a point where a number of things are happening at the same time. The average age of an appraiser has to be in the range of 60 to 65. That’s retirement age. On top of that, depending on who you talk to, 10 to 25 percent of appraisers could cease doing mortgage work because of UAD 3.6 alone. How many will ultimately adapt to the new form? How many will come back after sitting it out? We’ll see. But I’m more concerned about the lack of new people getting into the business than I am about the people who might leave.”

That concern is grounded in a number that rarely surfaces in the profession’s workforce discussions: since 2009, the number of first-time appraiser test takers has dropped 70 percent, Park reports. Park places the blame squarely on the Appraiser Qualifications Board, which he says has spent years creating unsupported barriers to entry rather than setting realistic minimum competency standards.

“Making the qualifications criteria realistic is what the AQB’s job has always been,” Park says. He continues: “I’m afraid they’ve lost their way. A national profession that has only a few hundred new people coming in a year is not a profession that’s going to be around for long. Do we have enough appraisers right now? Maybe. Probably in certain areas. But mortgage lending is at its lowest level in decades. If we have any significant increase in mortgage volume, the appraiser community is going to have a really hard time keeping up. Appraisers aren’t Doritos®. You can’t just go out and make more. It takes three to five years, and in today’s market, that’s a generation.”

That pipeline collapse has consequences. When mortgage demand spikes and appraisers can’t keep up, lenders and regulators look for alternatives. “So few new entrants over the last 10 years has led to a backstop, which is technology,” Park says. “Regulators are not going to allow appraisals to go back to $2,000 and a two-month turn-time to complete. The industry needs to work together to figure out how it evolves, and that includes getting more people into the business with different types of qualifications and backgrounds.” To make matters worse, Park says the profession may be running out of time to make these critical reforms.

Park’s concern is backed by exam data. According to CRN research, the number of first-time appraiser test takers has fallen from 4,790 in 2009 to 1,421 in 2025. Of those, just 820 passed; roughly 15 new appraisers per state. The Licensed Residential exam, which serves as the entry point for most new appraisers, saw test taker volume drop 62 percent between 2022 and 2025 alone.

“The appraisal community should be focused on what’s next,” Park says. “The system for how appraisals are completed and used in mortgage lending is essentially the same as it was in the 1930s. There’s plenty of data now, there’s plenty of computing power, and AI makes the need for change even more real. The whole mortgage lending process is going to change, with or without appraisers. If we don’t get more people into the business who are thinking about different ways to do things, it becomes a self-fulfilling prophecy. Appraisers will either evolve with what’s coming, or they won’t.”

For the AQB’s part, it is worth noting that they are currently considering changes to the Real Property Criteria. In December 2025, the AQB released an exposure draft proposing changes to the Criteria, accompanied by two concept papers exploring a “Skills Based Pathway” and an “Examination Only Pathway” to credentialing. The comment period closed in March 2026. Whether these proposals result in meaningful reform or follow the slow, incremental pattern of past AQB revisions remains to be seen.

(story continues below)

(story continues)

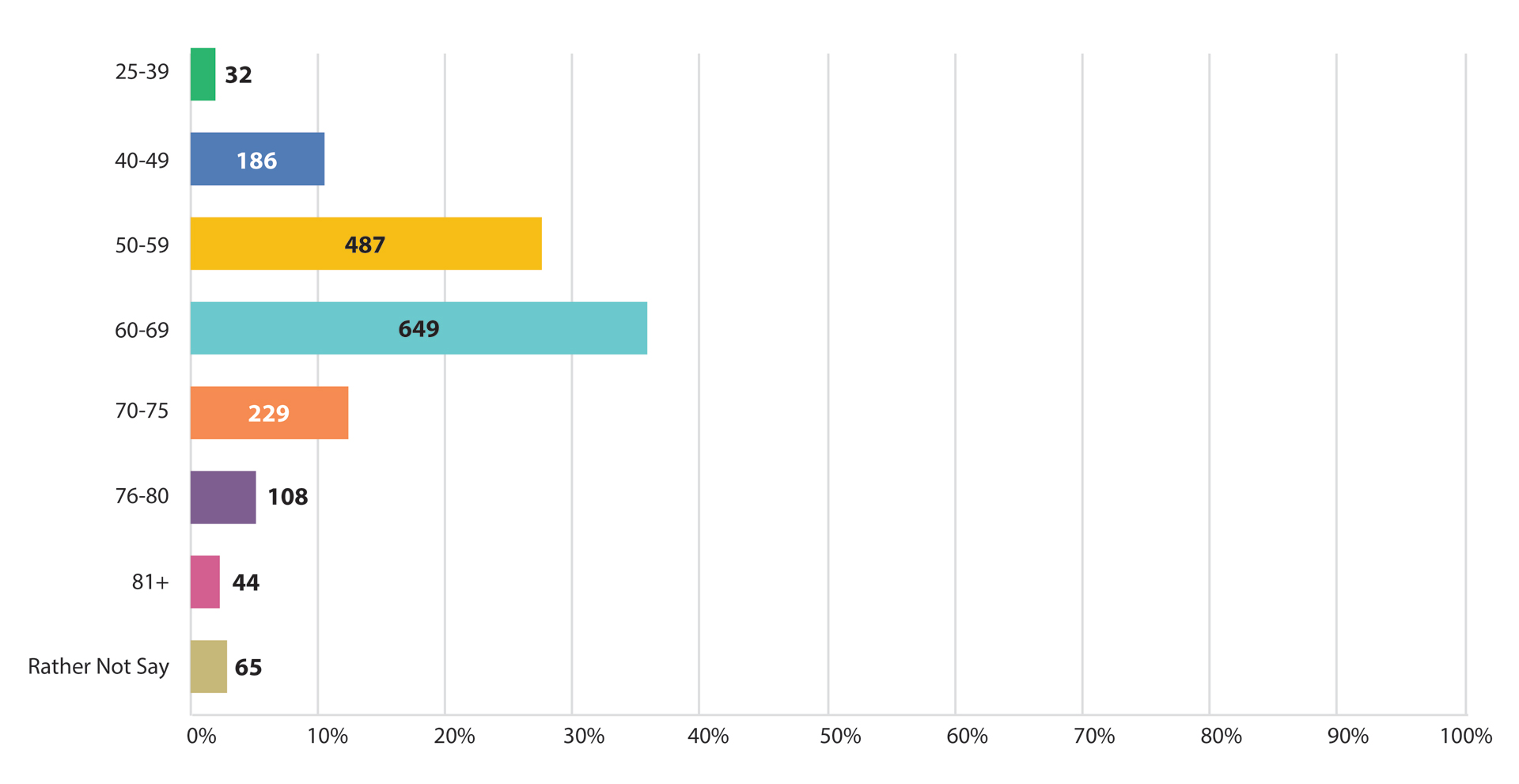

Age Demographics

Roughly 57 percent of active appraisers in our survey are over 60 years old. At the other end, less than two percent of respondents are between 25 and 39.

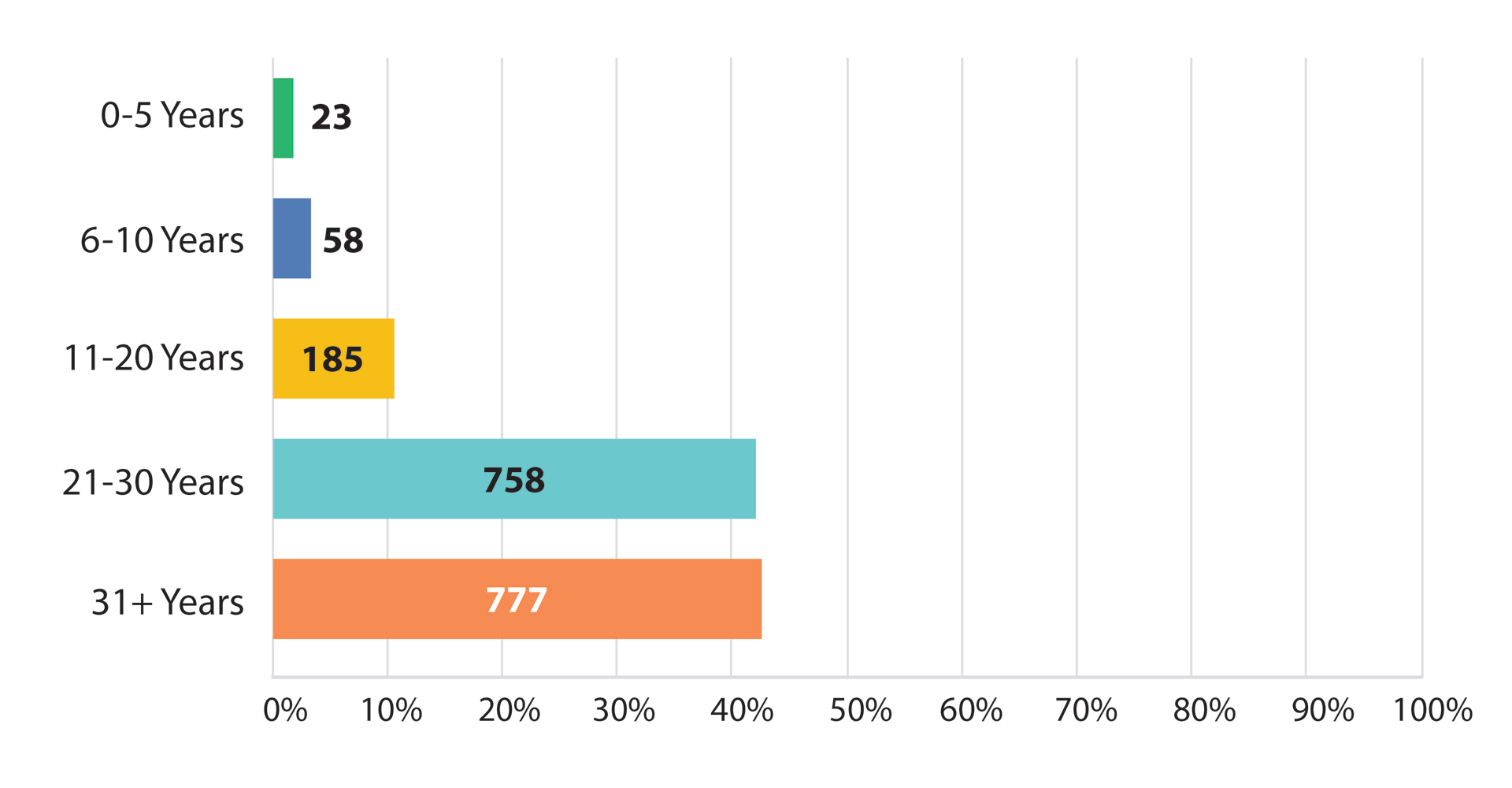

On experience, the numbers are equally striking. Of respondents, over 43 percent have been appraising for 31 years or more, and 42 percent for 21 to 30 years. Just over one percent of respondents have five years of experience or less. The profession has never been older or more experienced than it is right now. And it has never been harder to find a new appraiser entering the field. (Working RE‘s readership skews toward experienced, long-tenured appraisers, and these figures likely trend slightly older than the profession as a whole.)

UAD 3.6: The Readiness Gap

The November 2, 2026 mandatory compliance deadline for UAD 3.6 is roughly four months away. While Working RE‘s survey ended March 15 (three months prior to this publication), even if we account for a rapid ramp up, the data suggests that the profession is not ready.

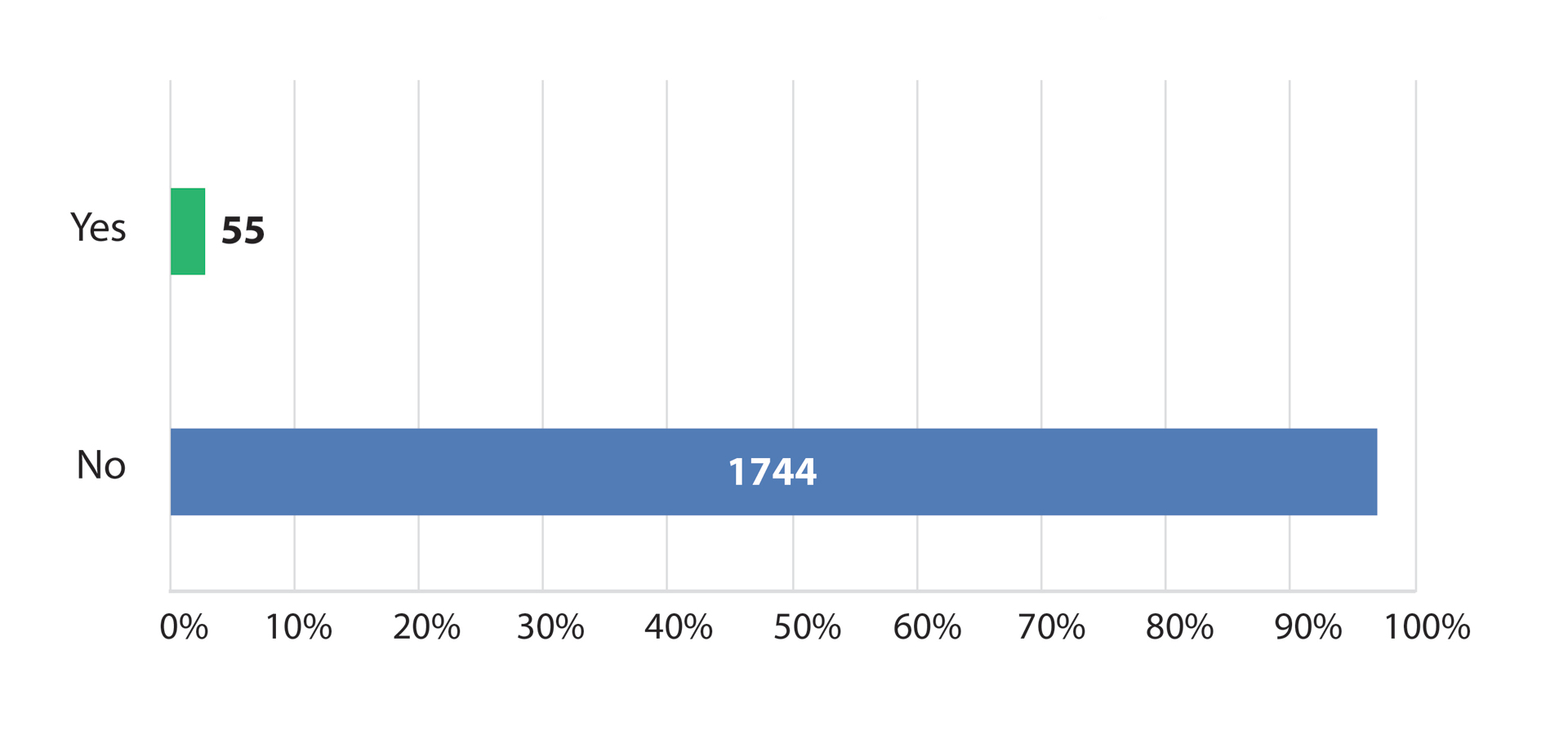

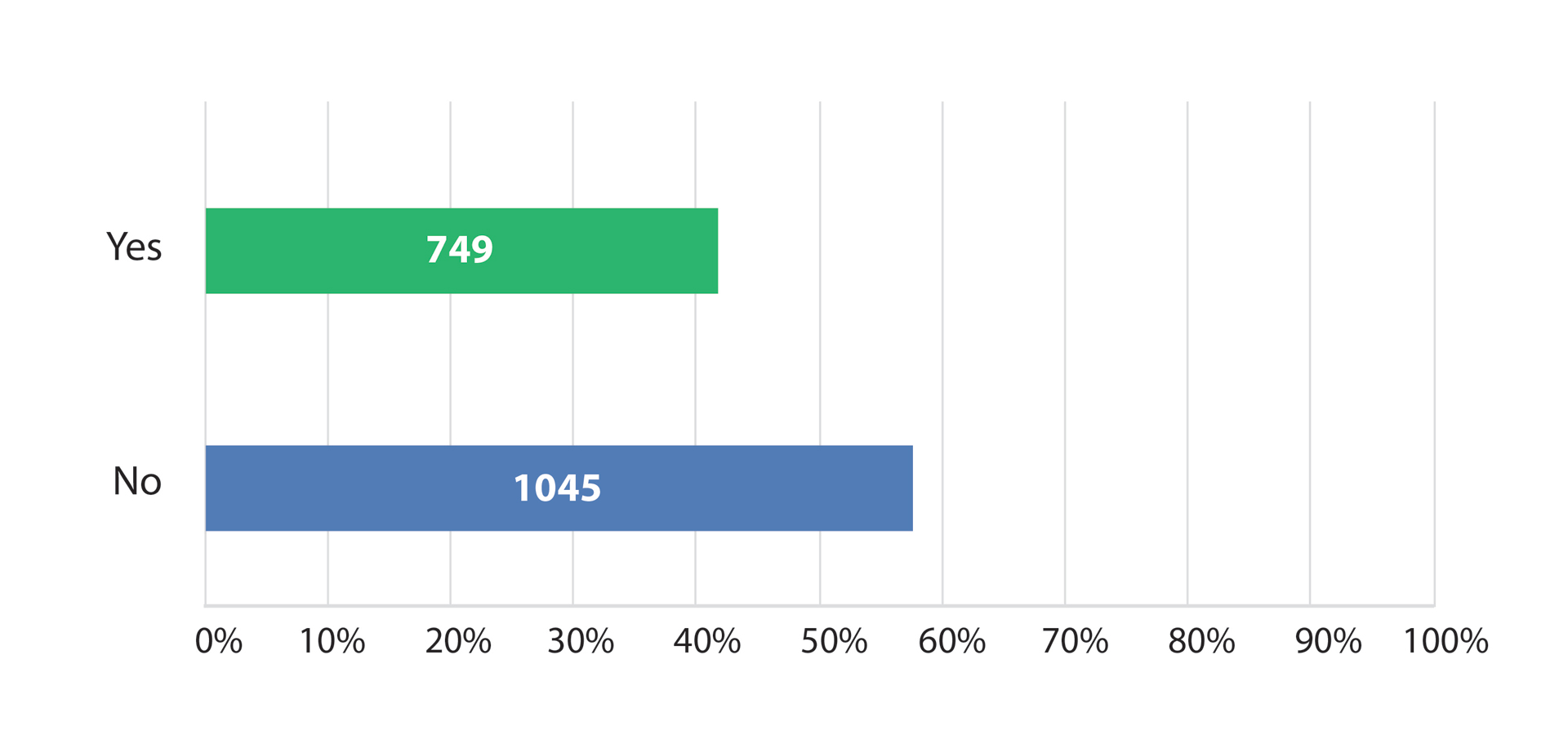

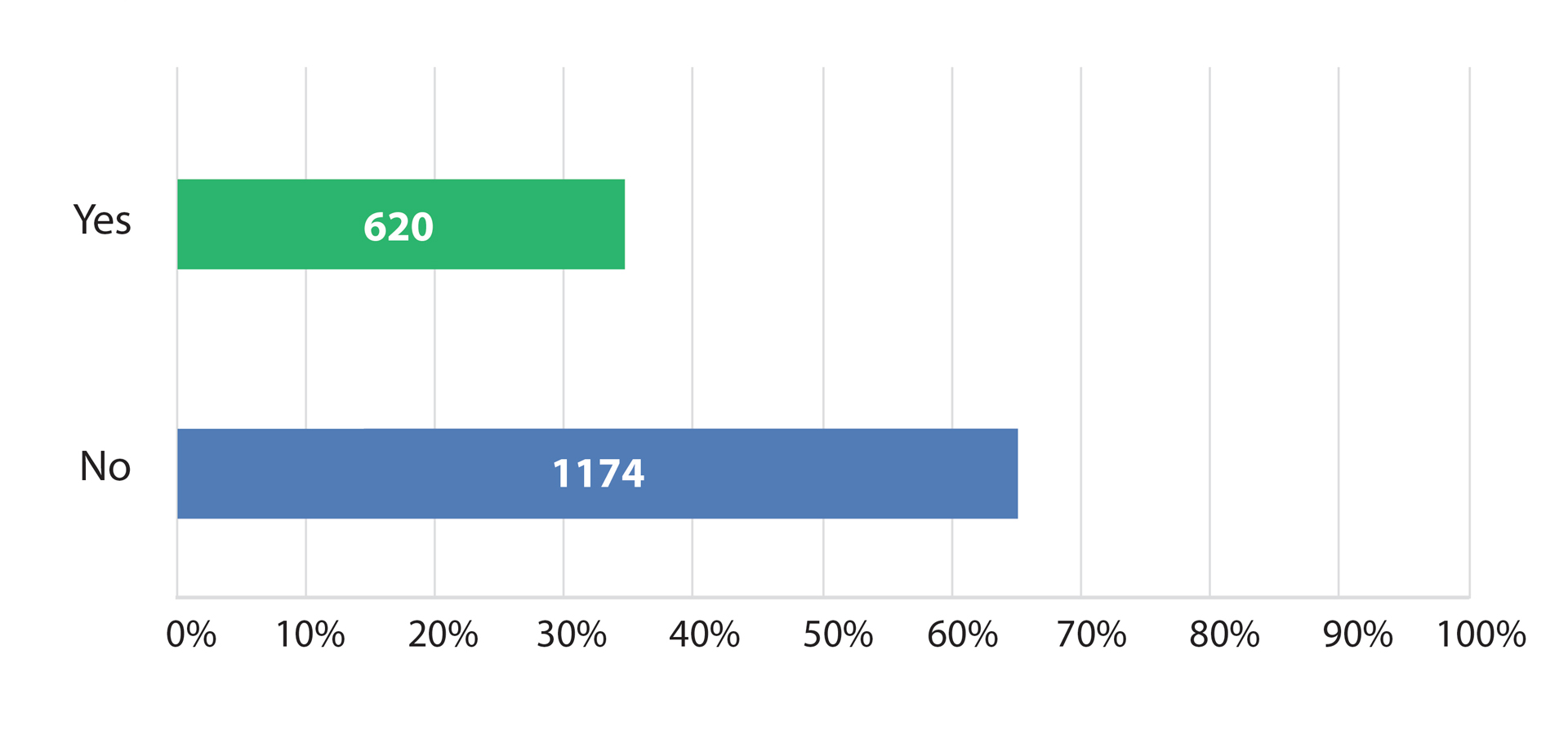

Only three percent of respondents—55 out of 1,798—had completed an appraisal using the new UAD 3.6 format. Meanwhile, 58 percent had not yet taken the 7-hour training course that Fannie Mae and Freddie Mac developed specifically for this transition. That means close to six in 10 appraisers are approaching a mandatory form change with no training and no hands-on experience.

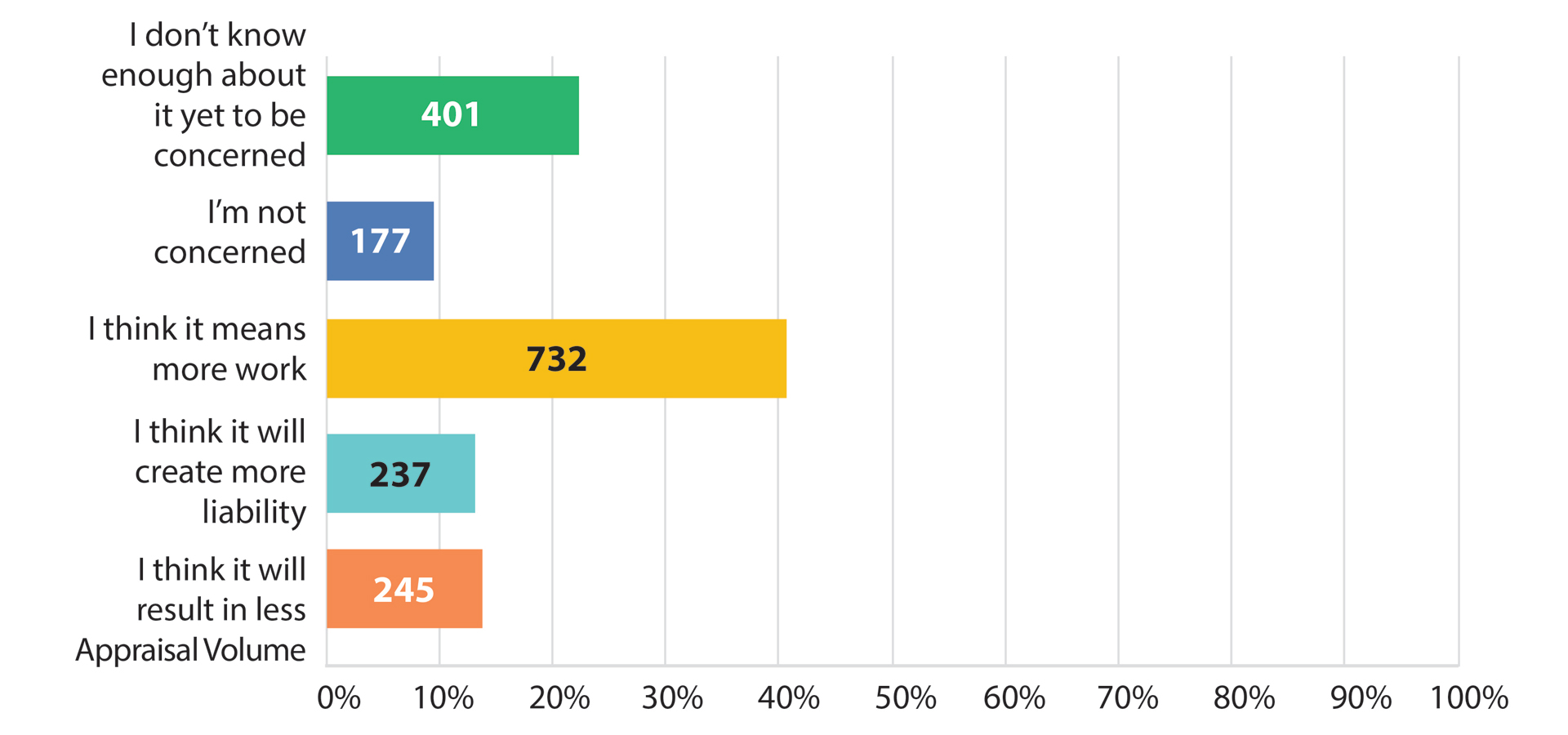

The primary concern about UAD 3.6, selected by 40.87 percent of respondents, is that it means more work. Another 13.68 percent believe it will result in less appraisal volume, and 13.18 percent are concerned about increased liability exposure. A notable 22.39 percent say they do not know enough about it yet to be concerned—which may be the most clarifying data point of all. Nearly a quarter of the profession is less than six months from a mandatory compliance deadline and has not yet engaged with what the change actually entails. Only 9.88 percent are not concerned.

On UAD 3.6 readiness specifically, Park says the rollout data he has seen is worrying. At a Cotality-hosted industry event in Dallas in mid-March, organizers had expected to report on hundreds of UAD 3.6 loans processed through the system nationally. The actual count at that point was a handful.

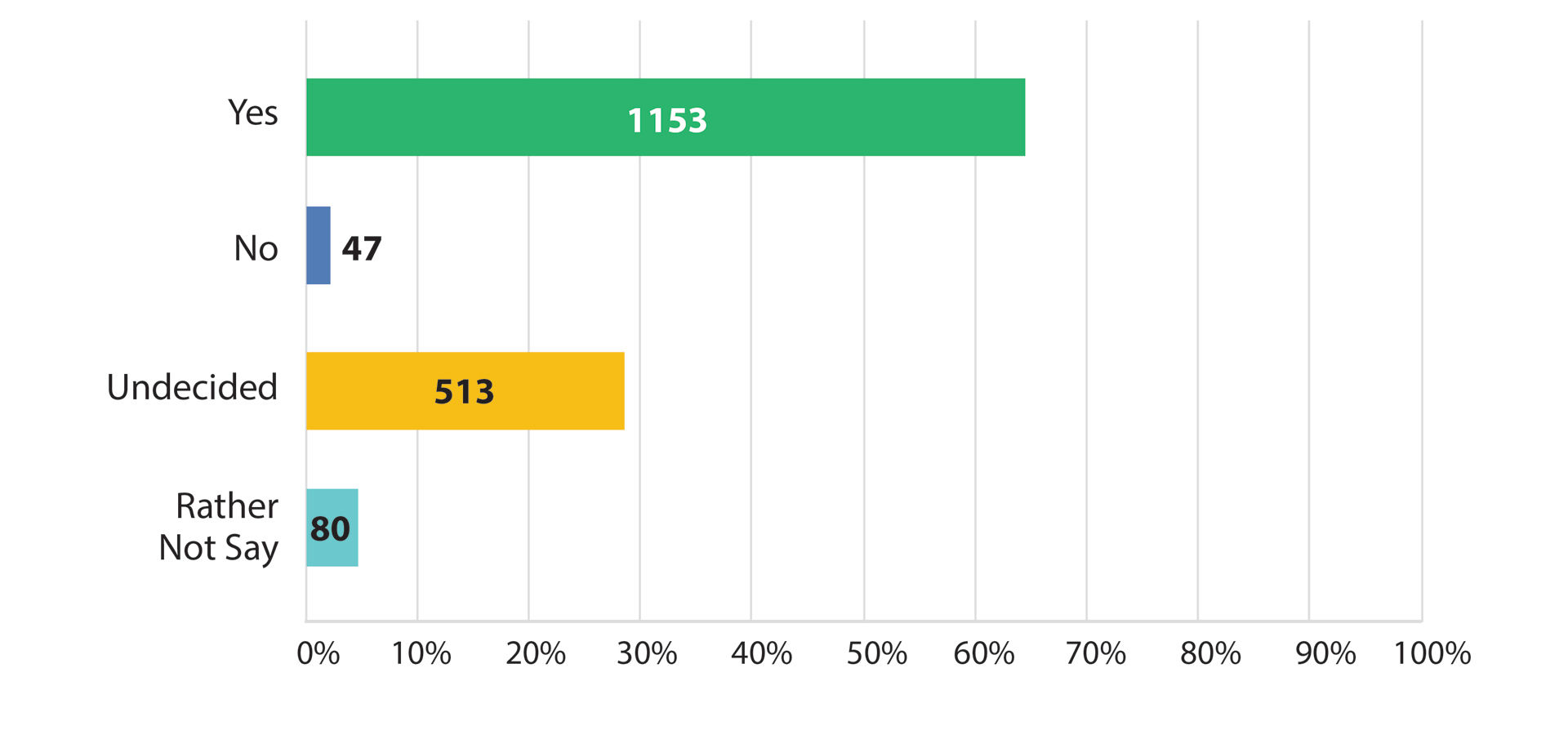

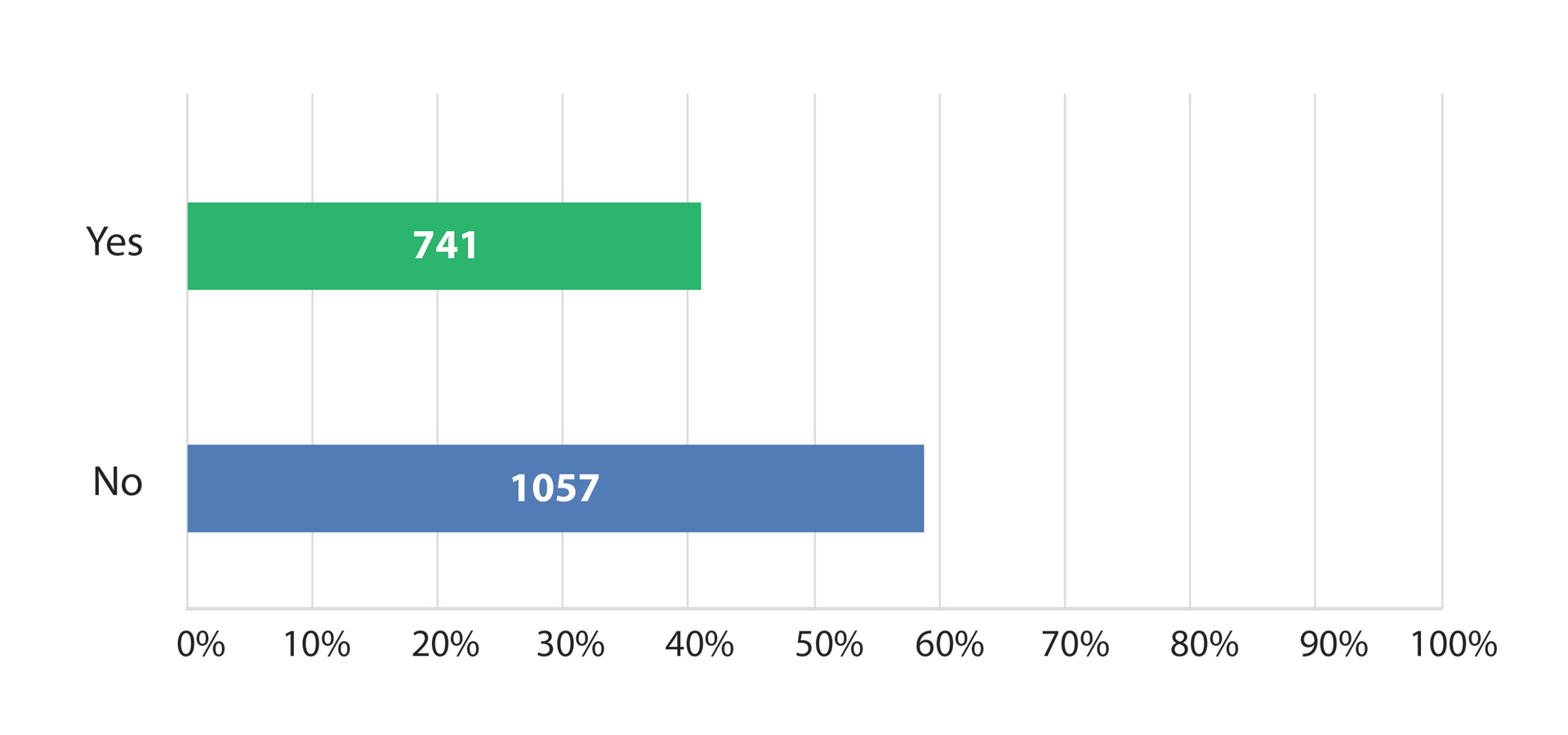

For lenders and appraisal management companies watching this rollout, the fee data is worth noting. Of respondents, 64.29 percent plan to increase their fees for UAD 3.6 assignments. Only 2.62 percent say they will not. The more-work concern and the fee increase intention are directly linked. Appraisers who anticipate a heavier lift are pricing accordingly. Whether AMCs and lenders absorb those increases or push back on them is a market dynamic that will play out over the next twelve months.

The liability question is real. The new URAR introduces more data fields, more structured property description requirements, and more points of potential dispute. UAD 3.6 requires appraisers to rate interior and exterior quality separately, document appliance functionality, and provide more detailed, field-specific updates than the legacy 1004 form required.

“More fields mean more opportunities for errors, omissions, and inconsistencies. Especially as it relates to comments and fields about home systems’ functionality and condition,” says Brianna Walker, Senior Underwriter at OREP Insurance. “It’s too early to say whether UAD 3.6 will generate a measurable increase in E&O claims, but the structural conditions for it are there. We’re watching the early adoption data closely, and as claims patterns emerge, we’ll share what we’re seeing with OREP’s Members and give them advice to navigate it, including disclaimers.”

(story continues below)

(story continues)

Hybrid Assignments: Resistance Holds

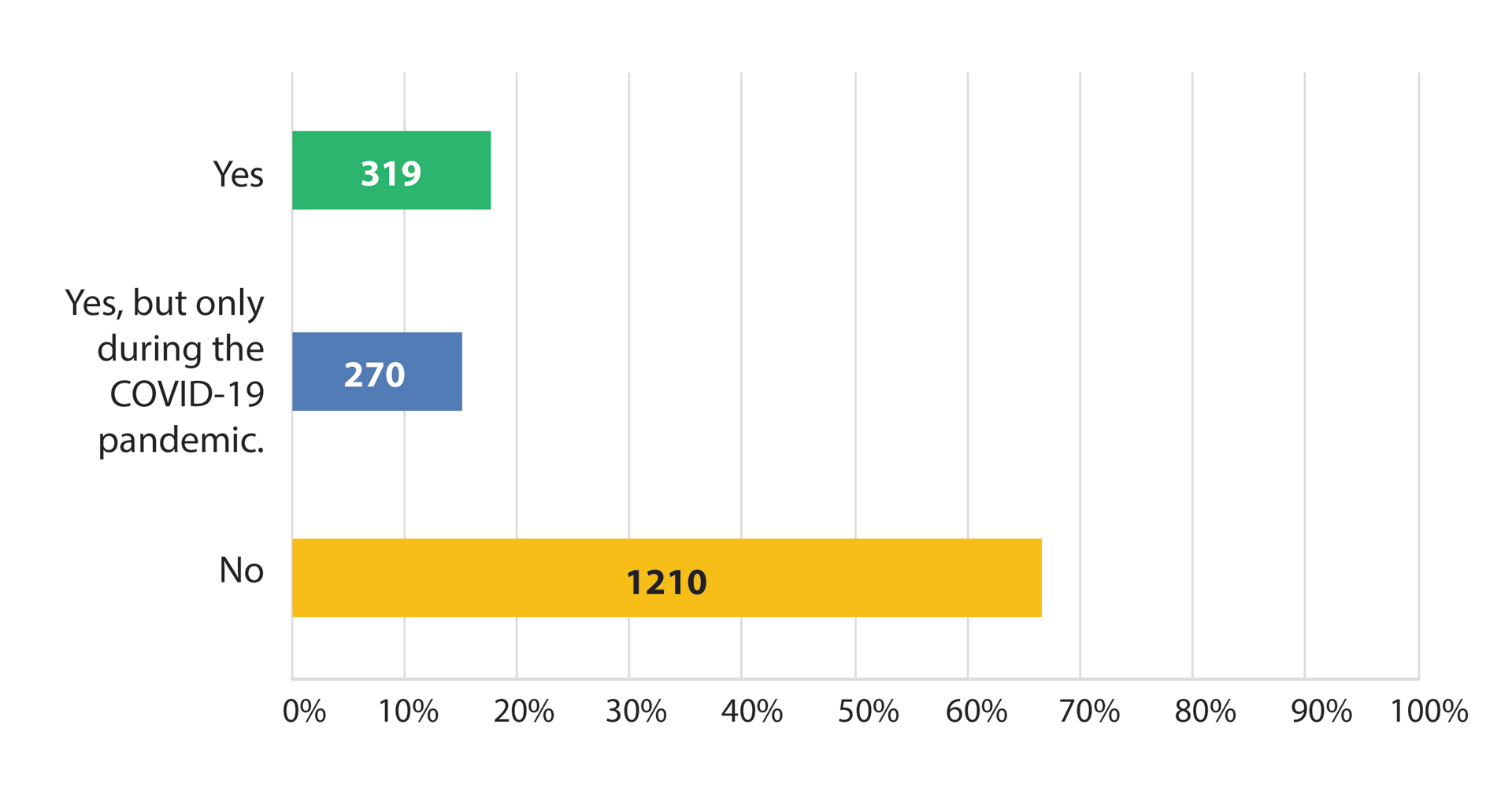

The profession’s skepticism about bifurcated and hybrid appraisals has not softened. Of 1,798 respondents, 67.30 percent have never done a hybrid assignment. Another 15.02 percent did hybrid work only during the COVID-19 pandemic; a period of necessity rather than choice. Only 17.69 percent have done hybrid work as a regular practice. Looking ahead, 65.48 percent say they are not open to hybrid assignments in the future.

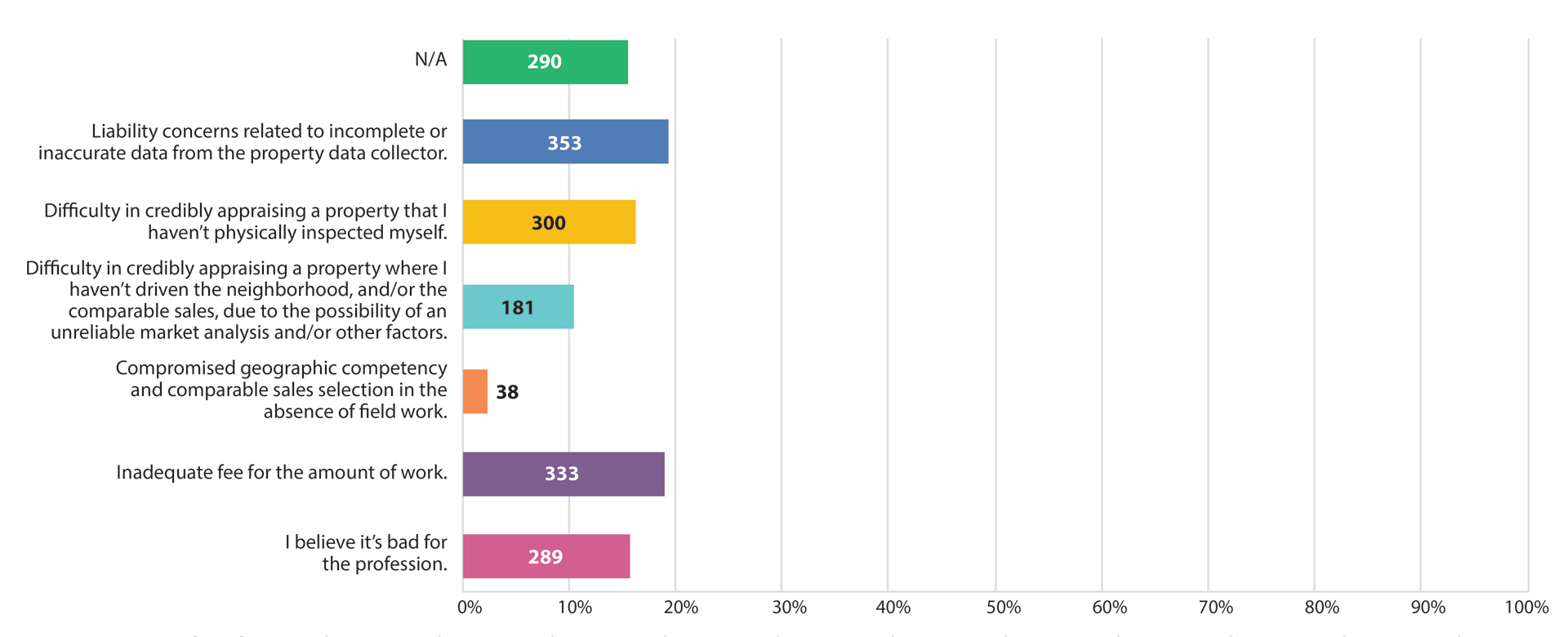

The reasons are professional objections, not technophobia. Liability concerns about incomplete or inaccurate data from the property data collector rank among the top barriers to acceptance. Alongside them: the fundamental difficulty of credibly appraising a property the appraiser has not physically inspected, and the geographic competency problem, i.e. that a credible market analysis depends on having driven the neighborhood and the comparable sales, not just having access to MLS data.

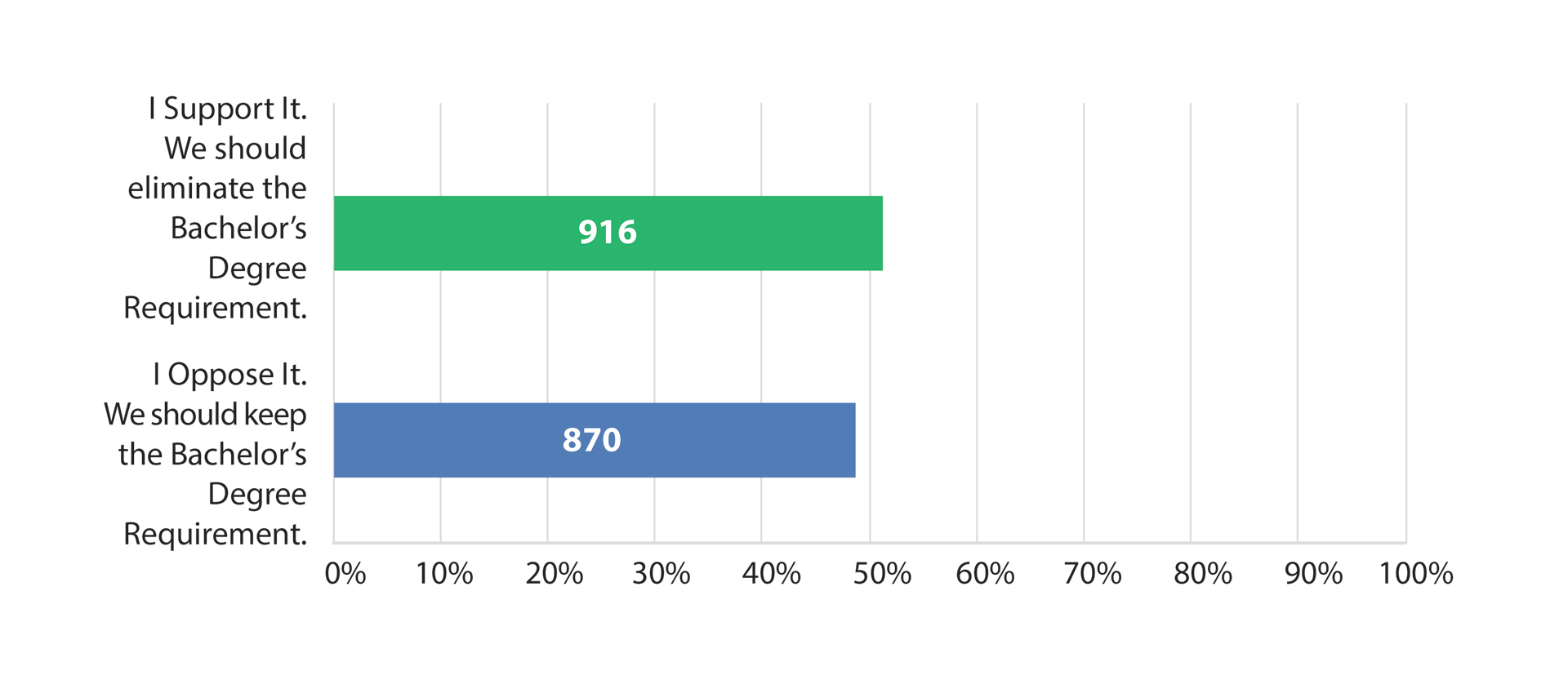

The Degree Debate: A Divided Profession

The 2026 survey found the profession nearly split on whether the bachelor’s degree requirement for Certified Residential appraisers should be eliminated: 51.29 percent support removing it and 48.71 percent oppose. That is a significant shift from Working RE‘s 2016 survey, when roughly 80 percent of appraisers opposed the degree requirement in some form. It’s hard not to wonder whether appraisers’ responses have been influenced by the incredibly low volume they’ve faced in the last few years.

AI Adoption

AI tool adoption among appraisers is higher than many in the profession might expect, but still lower than what’s reported in the general public. Of 1,797 respondents, 41.24 percent report using AI tools in their business, with ChatGPT cited as an example.

The Takeaway

Taken together, the 2026 survey describes a profession that is older and more experienced than it has ever been. Appraisers remain skeptical of hybrid products, divided on credentialing, and approaching one of the most significant form changes in decades largely untrained. The retirement numbers are alarming on their face but unconvincing as a cliff narrative. Working RE‘s own historical data makes that case directly.

What the 2026 data cannot tell us is whether UAD 3.6 will finally push appraisers into retirement in a way that past challenges failed to do. The new form demands a genuine workflow change, not just a reporting update. Most appraisers plan to raise their fees accordingly. Whether they get those increases, or whether this becomes the pressure point that finally turns retirement plans into actual retirements, is the story Working RE will be tracking over the next twelve months. (See the full 2026 survey results below. Survey closed March 15th.)

1. What’s Your Opinion on the Appraisal Qualifications Board’s (AQB) proposal to do away with the college degree requirement for Certified Residential?

2. What is your primary concern about the new UAD 3.6?

3. Have you done any appraisals using the new UAD 3.6 format yet?

4. Do you plan to increase your appraisal fees for UAD 3.6 appraisal assignments?

5. Have you completed the new 7-Hour Class on Fannie Mae / Freddie Mac’s UAD 3.6 yet?

6. Are you open to doing Hybrid appraisal assignments in the future?

7. Are you using any artificial intelligence tools in your business? (ChatGPT, for example.)

8. Have you done a Bifurcated/Hybrid appraisal assignment as the Appraiser Analyst?

9. Please select the reasons for not accepting assignments as the Appraiser/Valuation Analyst only:

10. How old are you?

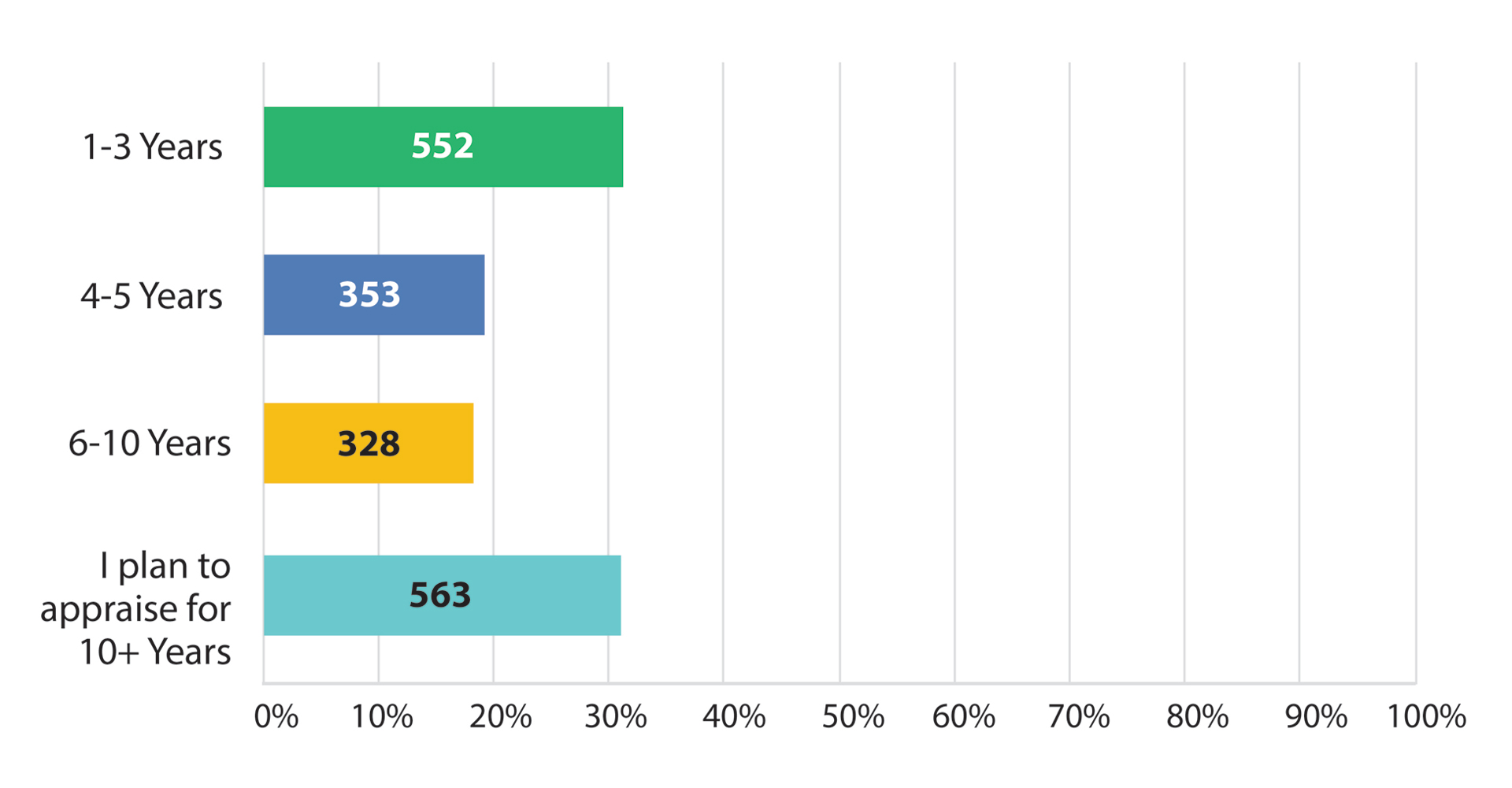

11. Do you plan to leave or retire from the appraisal profession in the next:

12. How long have you been appraising?

About the Author

Isaac Peck is the Publisher of Working RE magazine and the President of OREP Insurance, a leading provider of E&O insurance for real estate professionals. OREP serves over 10,000 appraisers with comprehensive E&O coverage, competitive rates, and 14 hours of CE at no charge for OREP Members (CE not approved in IL or AK). Visit OREP.org to learn more. Reach Isaac at isaac@orep.org or (888) 347-5273. CA License #4116465.

by Doug

It’s not just the education requirements. It is the education requirements AND the low fees. By that I mean someone who is young needs to make a good living to pay for school loans, etc if they have a Bachelor’s degree. The death of the industry was the HVCC and AMC model. You can thank Cuomo for that.

-by Retired Appraiser

If you are still an appraiser after 16 years of this horse ship you fall into one of two catagories: You are either a dip ship or a dumb ship.

-by Charles Haley

lThe last appraisal I paid for was fraught with errors, leaving much to be desired. I truly believe we would be better served with Automated Valuation Models (AVMs), which offer a more reliable and efficient alternative.

-by Bryan R.

This article is well-written. By distinguishing the AMC fee and the Appraiser fee from the Total Appraisal fee, it highlights issues within the AMC bidding process. Appraisers are being forced to undercut each other to a point where their compensation is disproportionate to the work involved and the potential future liability they assume. When involving an AMC, it may be appropriate to mandate that a “Customary and Reasonable” percentage of the total appraisal fee is actually paid to the Appraiser, potentially around 65-70%? If the fee paid to the Appraiser by the AMC was predetermined, the bidding process would be limited to turn-time. This would prompt AMCs to assign orders to their most qualified appraisers and utilize their business acumen to provide quality appraisals to clients while reducing operating expenses.

-by Mary Cummins

Great article. That is exactly what’s happening. Many times a client will say “I paid $900-$1,500 for the appraisal” when the appraiser is only getting $350-$450 for large complex homes and multifamily properties. Not fair for the consumer or appraiser.

-by Rich Bryan

Having done appraisals for over 40 years, I never train a person to be an appraiser unless they have been a Realtor for several years. An appraiser is a Market Reporter. If you have not actively helped a buyer and / or a seller locate, purchase and finance a house, how can you report the actions of a buyer / seller market participant. Non Realtors just don’t know the concerns of the buyer / seller clients. This means that the non Realtor appraiser does not know the concerns of the the mortgage holding client and / or ultimate appraisal user.

-by Wendy Stedman

I really like the idea of adding RE Sales experience as a requirement. As a Realtor and Certified Appraiser… I completely agree with your policy

-by Doug

I would agree to a point. I have tried to train a few real estate agents. They were horrible. They couldn’t analyze a property and just were not detail oriented. People that are good agents tend to be more extroverts than analytical. And frankly a good agent can make more money selling real estate than appraising. Biggest mistake I made was to stop selling real estate along with doing appraisals. But I hated working weekends with kids in high school.

-by Alex P

I agree with everything you are pointing out.

-