|

> Fannie Mae > AMC Resource Guide> OREP E&O ★★★★★ “They are knowledgeable, professional, and understand urgency.” – Joe Thweatt |

2026 Market Update: Appraisal Volume, Waivers, and PDCs

by Isaac Peck, Publisher

For the last several years, the appraisal profession has been described as being “at a crossroads.” In reality, very little has fundamentally changed. Volume remains constrained, appraisal waivers persist, and property data collections continue to grow slowly—but not dramatically.

The housing market has cooled significantly from the pandemic-era surge. Policy changes, higher interest rates, and affordability pressures have slowed transaction volume, while automation tools like appraisal waivers and PDCs continue to expand at the margins. Appraisers are operating in a market that is more constrained, more competitive, and less forgiving than it was just a few years ago.

The question now is how the new tools being thrown into the market are changing the way the proverbial garden is being tended. Automation and appraisal waivers are like sprinklers and shortcuts, touted as efficient, but much less hands-on. For appraisers, 2025 has not brought a meaningful rebound. Volume remains flat, while pressure from waivers and PDCs continues to build.

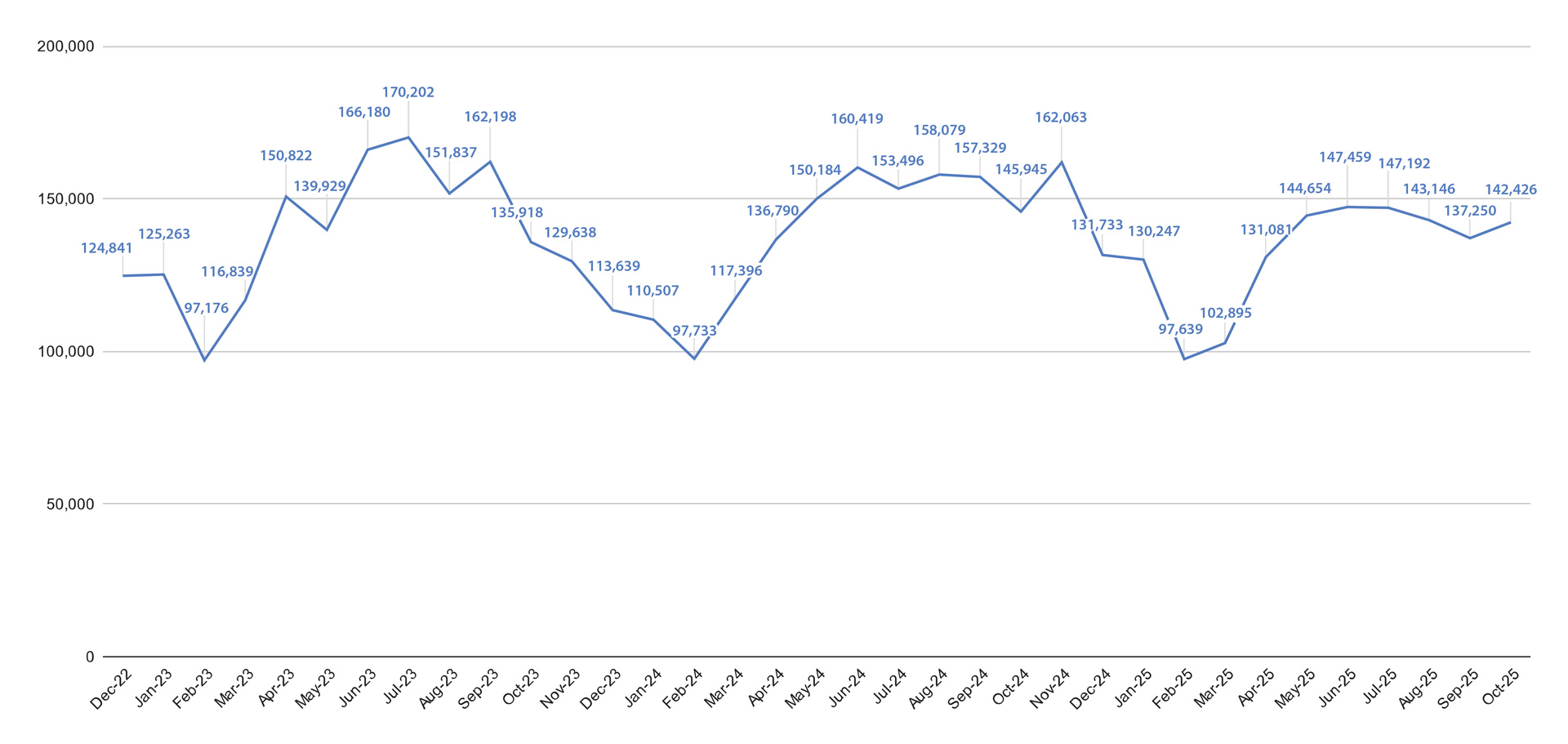

Appraisal Volume: Flat, Seasonal, Still Constrained

Residential appraisal activity remains well below the boom years of 2020 and 2021, as high mortgage rates continue to keep many homeowners locked into lower loans and dampen refinancing. In practical terms, 2025 looks much like 2023 and 2024: flat volume and no meaningful rebound. See Figure 1: Appraisal Volume for a visual representation of the last three years. Note that these numbers represent actual appraisals and do not include waivers or PDCs.

Figure 1: Appraisal Volume

Regional patterns remain uneven: some counties posted small declines in sales, while others saw modest gains. Buyer urgency has cooled, with homes spending longer on the market, which in turn demands sharper analysis and stronger justification from appraisers when making adjustments. At the same time, AVMs and hybrid valuation products continue to gain ground, modestly reducing the share of assignments going to traditional appraisers.

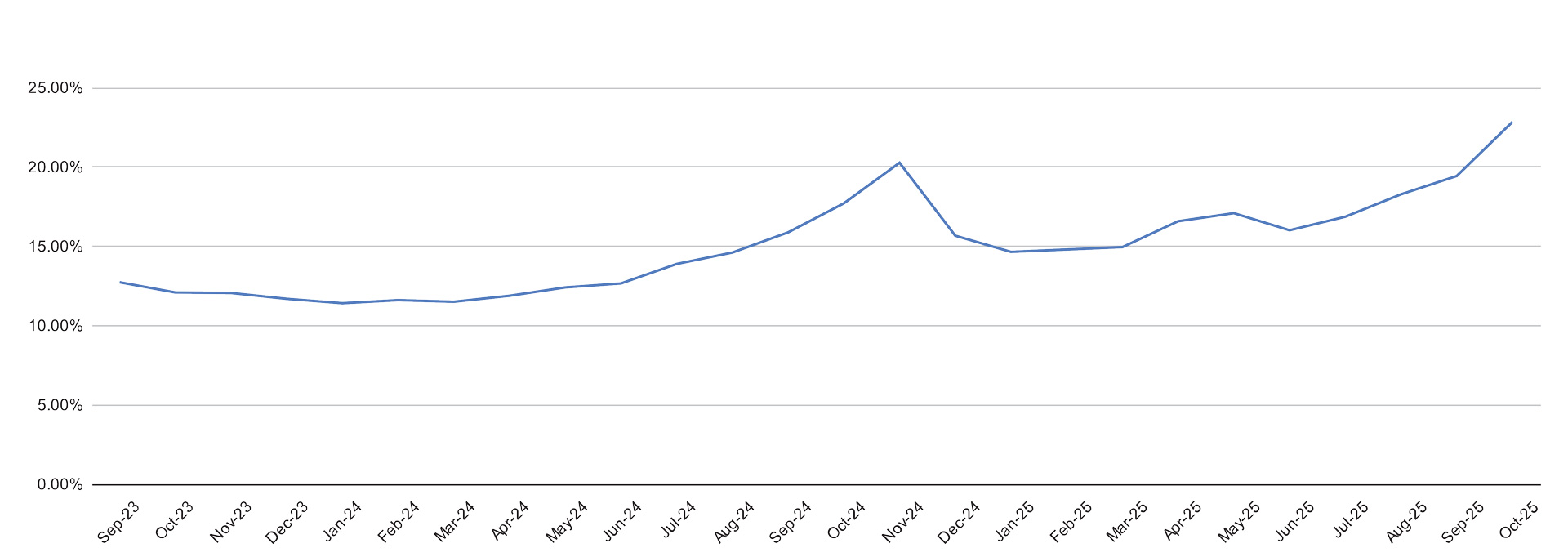

The Rise (and Plateau) of Appraisal Waivers

The use of appraisal waivers by the GSEs remains elevated, but the data does not support the idea that waivers are accelerating unchecked or fundamentally displacing appraisers.

According to the AEI Housing Center’s October 2025 update, appraisal waivers were used on roughly 23 percent of GSE loans that month. (See Figure 2: Appraisal Waivers as a Percentage of Loan Volume) While that number is meaningful, it is still far below the pandemic-era peak in 2021, when waivers accounted for nearly half of all loans. In other words, waiver usage today is elevated compared to historical norms, but well off its high-water mark.

Figure 2: Appraisal Waivers

It is also important to understand how waivers are being used. Waivers tend to cluster around lower-risk, highly standardized transactions, particularly refinances or loans with low Loan-to-Value ratios where automated models and existing data give lenders more confidence. This is not a new development, nor is it evenly distributed across property types or markets.

Programs like Freddie Mac’s ACE+ Property Data Report and Fannie Mae’s Value Acceptance + Property Data have expanded the GSEs’ ability to offer waiver options. For appraisers, the takeaway is not reassurance; it is clarity. Waivers reduce demand at the margins, but they do not eliminate the need for appraisers. What they do reinforce is the importance of positioning appraisal services where automation falls short: market nuance, property complexity, adjustment support, and accountability. Complex properties, atypical markets, layered risk profiles, and loans requiring judgment continue to require full appraisals. In practice, that has not changed.

(story continues below)

(story continues)

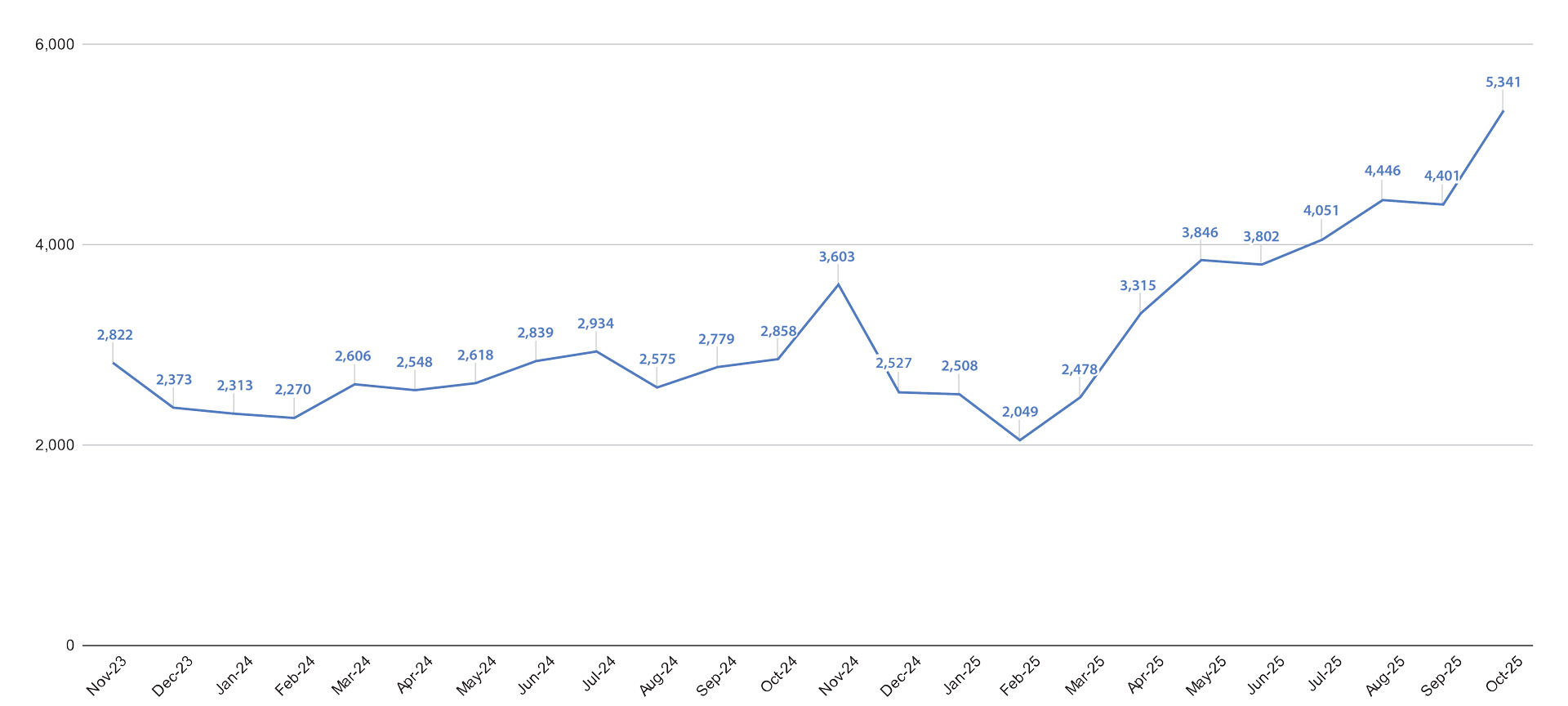

PDCs Slowly Ticking Up

Two years ago in these pages, we noted that while property data collections were being heavily promoted, actual GSE adoption remained extremely limited. (Read “Appraisal Volume, Waivers and Property Data Collections.”)

Since then, the picture has become a little more complicated—but not nearly as dramatic as some headlines suggest. See Figure 3: Waivers + PDCs for a graphical representation.

Figure 3: Waivers + PDCs

At the end of 2025, AEI data shows that full appraisals remain dominant. Even with slightly expanded eligibility and continued promotion by the GSEs, PDCs still represent only a small fraction of total valuations. Depending on the month, PDCs account for roughly two to three percent of GSE transactions, a meaningful increase from prior years, but far from a large-scale replacement of traditional appraisals.

It’s important to note that the data we have on PDCs is specific to when they were used in conjunction with an appraisal waiver. Right now we do not have good data on how many PDC plus appraisal desktop appraisals are being conducted every month (this is commonly referred to as a hybrid appraisal).

For appraisers, the takeaway is nuanced and cautionary. The eligibility box for PDCs is already broad, yet lender adoption has lagged well behind what many predicted. It suggests the current limits on PDC volume are less about policy restraint and more about operational friction and lender risk tolerance. Full appraisals continue to dominate not because PDCs are narrowly defined, but because many lenders are still unwilling or unable to deploy them at scale.

A Market in Slow Motion

Still, we should talk about those market shifts. The housing market was not a lush, high-growth garden in 2025, but it’s not dead. Metro cities (with some exceptions) have mostly posted declines, inflation has slightly outpaced housing gains, and affordability is not just a catch phrase: Elevated mortgage rates and high ownership costs continue to suppress demand.

The most telling statistic is that more than half of closed sales nationwide in November involved price reductions. That’s the highest share in almost four years. There’s also a growing perceived disconnect between appraised values and actual sale prices, with lenders and borrowers complaining about “over‑appraisals.” Appraisers can certainly do some things to mitigate this, like sharpening comp selection and making market condition adjustments. But this is also an opportunity to lean into real‑time data that reflects what the market is doing and what buyers are willing to pay.

Economic indicators mix optimism about long‑term housing demand with caution about near‑term affordability. Employment remains strong, but inflation and interest rates weigh heavily on buyers.

Appraisers cannot control interest rates, affordability, or broader market conditions. What they can control is how they respond: by using better data, sharpening analysis, and adapting workflows where appropriate. Those steps won’t restore pandemic-era volume, but they do position appraisers to remain relevant and credible in a slower, more selective market.

Waivers and PDCs are not disappearing, but the data shows they remain limited in scope and concentrated in lower-risk assignments. Full appraisals still dominate when complexity, judgment, and accountability matter most. In that environment, appraisers who understand where the market actually is—and adjust their businesses accordingly—will be better positioned to weather the cycle and compete for the work that remains.

As market conditions shift, appraisers should also review their insurance coverage. For a comparison of the top appraiser E&O providers and current pricing, see our best appraiser E&O insurance guide.

About the Author

Isaac Peck is the Publisher of Working RE magazine and the President of OREP Insurance, a leading provider of E&O insurance for real estate professionals. OREP serves over 10,000 appraisers with comprehensive E&O coverage, competitive rates, and 14 hours of CE at no charge for OREP Members (CE not approved in IL and AK). Visit OREP.org to learn more. Reach Isaac at isaac@orep.org or (888) 347-5273. CA License #4116465.

by Brad Bassi

Mr. Glickman if that is correct, then here we go again. Seems that the GSE’s always like tweaking with things. One time they say it is about the data and borrower risk then the lower the credit score, isn’t that increasing the risk by adding borrowers who don’t carry the same risk level as a 750 score. Just weird, interesting and typical.

-by Jim Glickman

According to one AMC/PDC vendor I spoke to last fall, as of 10/15/2025 the minimum borrower credit score for a Waiver+PDC was lowered from 750 to 688. Perhaps that contributed to the sharp increase for October 2025 in Figure 3.

-