|

“One of the best courses that I have had in 17 years!” -Amy H.> Switch to OREP E&O Insurance: Enjoy Free 14 Hours of Free, Approved Continuing Education |

>> Take OREP/Working RE’s Bifurcated Appraisal Survey

Bifurcated Appraising

by Isaac Peck

Leaders within the appraisal community have long prepared appraisers that “change is coming,” and that the role of the professional appraiser is going to evolve in the coming years. Today, that change is here.

Fannie Mae has been extensively testing a new bifurcated valuation approach that breaks the appraisal process in two: data collection and then an analysis, if required.

Fannie has spent the first half of 2019 detailing its plans to roll out the 1004P, a new desktop appraisal that will be based on a Property Data Collection report that is prepared by a third party inspector; this is part one. Fannie has indicated that it is currently testing appraisers, appraiser trainees, insurance inspectors, real estate agents, property preservation service professionals, and smart home service professionals as potential Property Data Collectors to determine “which labor force can best collect data,” including a “robust and accurate set of data elements, photos, and floor plan.”

The more impactful revelation is that Fannie aims to replace the appraisal requirement completely where it can. In these scenarios, a property data collector, not necessarily a licensed appraiser, will inspect a home and report back on the condition of the property. Then, based on that property inspection report, a desktop appraisal may be ordered or the appraisal requirement might be waived altogether.

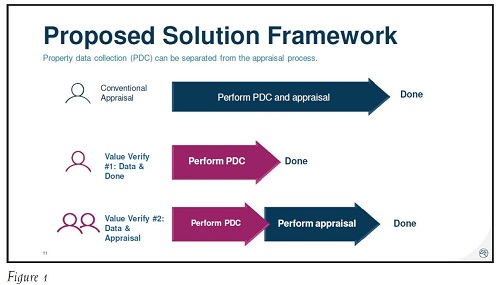

Fannie is calling its solution Value Verify, with the goal to separate the property data collection (PDC) from the appraisal process. Under Fannie Mae’s proposed plan, after a property data collector submits a report on the property’s characteristics and condition, Fannie Mae will decide if it wants to (A) accept the loan without any appraisal whatsoever, (B) require a desktop (hybrid) appraisal that uses the property inspection from the property data collector, or (C) seek out more information and perhaps order a full appraisal.

Figure 1 is a slide presented by Lyle Radke, Director of Collateral Policy at Fannie Mae, at the ACTS Conference in April, hosted by the National Association of Appraisers and Appraiser eLearning. It contrasts the conventional appraisal process, i.e. what is happening now, with the Value Verify model being proposed by Fannie.

While Fannie is currently testing a myriad of professions, in its June 2019 Appraiser Newsletter, it writes that “Appraisers are a natural fit for property data collectors. Let’s be clear: in our testing, appraisers are the primary providers of property data collection services, and we anticipate that will continue.” For those appraisers who are interested in getting work as a property data collector, Fannie writes that its process “requires new technologies (e.g., mobile apps, QC platforms, API connections) so appraisers need to have a technology partner. Several industry service providers have built the technology and are participating in the test. The best way to get involved is to affiliate with these companies. They are actively recruiting appraisers to provide property data collection services.”

We sat down with Radke to learn more about what Fannie is thinking, and what’s coming next.

WRE: What role does Fannie Mae see for licensed real estate appraisers, now and in the future?

Fannie Mae: Historically appraisers spend much of their time collecting data rather than developing a value opinion. With the enormous amount of data readily available today through the Internet and other sources, we anticipate the appraiser’s role will evolve into more of a market analyst and less of a data detective.

WRE: Fannie Mae has recently launched initiatives, such as Appraisal Waivers, Property Data Collection, and Hybrid Appraisals that make it appear there is a drive to minimize or eliminate the role of appraisers. Yet Fannie Mae has also recently launched initiatives (such as work with the National Urban League) to recruit individuals into the appraisal profession. How do you hope to recruit new appraisers while trying to minimize their role? Why would anyone want to be an appraiser when their role and income are obviously under such pressure? Is minimizing a step toward replacing?

Fannie Mae: In our June 2019 Appraiser Update newsletter, we discuss the role of a property data collector and how appraisers can fit into that role, given that they already perform property data collection as part of the traditional appraisal process. Appraisers already collect property data as part of the appraisal process, and many already have this skillset. Our intent is to raise the bar on the quality of collected data. Appraisers will be asked to collect data using more consistent standards than in the past. New technologies will help appraisers do this quickly and efficiently with fewer errors. We see tremendous opportunities in the future for appraisers who are quantitative, tech savvy, and nimble.

WRE: Fannie has said in the past there are around 40,000 appraisers sending appraisals through the CU/UAD system. Is that number about right?

Fannie Mae: When we look at data submitted through the Uniform Collateral Data Portal (UCDP), we see that the number of active appraisers fluctuates with demand. The biggest drivers of demand are seasonality, interest rates, and economic conditions. At peak volumes, we’ve seen about 45,000 active residential appraisers in UCDP while the trough is in the upper 30,000s. That range has remained stable over eight years since we launched UCDP. While we have not seen any large, persistent decline in the number of active appraisers during that time, we do see some flexible capacity. For example, some appraisers may specialize in other property types or other assignment types but, when demand is high, they pick up some residential work.

WRE: Do you foresee Fannie Mae (or the market) needing more than the current number of appraisers as the aging appraisers retire? Fewer? Why encourage new entrants?

Fannie Mae: The Appraisal Institute lists the median age of today’s appraisers at 60 years old, so we should expect substantial retirements in coming years. With fewer people entering the profession, we have to figure out how to attract a wider range of people to the field. With partnerships with other organizations, such as the National Urban League and the Appraisal Institute, we hope to raise awareness of career opportunities in the industry. We anticipate the nature of the residential appraisal will evolve to adopt emerging technologies and advanced analytics. New entrants will be expected to come up to speed with new technology and analytics.

WRE: What percent of all mortgages currently qualify for Appraisal Waivers, and how do you see that percent increasing or changing in the years ahead?

Fannie Mae: The appraisal waiver offering has not changed substantially in the past few years, but we are taking a very careful, deliberate approach in examining how technology can enhance the appraisal process, and we will closely examine any opportunities to responsibly achieve more efficient collateral risk management.

WRE: There has been a lot of discussion around the 1004P, Property Data Collectors, and hybrid appraisals. What is the objective of these initiatives? Who does it benefit?

Fannie Mae: Industry adoption of new technologies and processes can improve the quality of appraisals while providing substantial consumer benefits.

Examples of immediate benefits to the appraiser include enabling appraisers to specialize and become more efficient. Appraisers who prefer analysis over field work can choose to focus on valuation, while appraisers who prefer field work can specialize in that. There will still be many traditional assignments for the generalist as well.

WRE: One of the common arguments is that hybrid appraisals are faster than a traditional appraisal. Has your testing supported that hypothesis? By how much? Why do you think it’s faster? Do you think the business model of many AMCs to shotgun blast appraisal orders, sometimes shopping for a week or longer for the lowest fee appraiser, has something to do with delays in appraisal turn-times?

Fannie Mae: In the Value Verify framework, there are two possible outcomes: Data & Done and Data & Appraisal. When the process results in Data & Done, it reduces the cycle time by several days. That said, our purpose in requiring property data collection and appraisals is to help us manage our collateral risk exposure. The feedback we share with lenders about their appraisals is framed around quality, accuracy, and risk management. That is the purpose of Collateral Underwriter, our post acquisition loan reviews, and our Appraisal Quality Monitoring program. They enable us to hold lenders accountable if their business model results in inferior appraisal quality.

WRE: One of the criticisms of hybrid appraisals is that, by driving to and from the subject property and the comparables, appraisers often learn about the respective neighborhoods, construction types, community boundaries, as well as observe other factors which influence value, such as power lines, proximity to certain positive or negative sites or landmarks, etc. Fannie Mae currently requires appraisers to inspect all comparables used in the 1004. This not only helps keep the appraiser informed about the geographic area generally, but also provides specific information about what might be influencing value and what is comparable or not. Will Property Data Collectors be required to drive comparables or know the neighborhood?

Fannie Mae: The volume of information available to appraisers from the office has expanded enormously in recent years, including aerial imagery, street level imagery, three dimensional tours, and GIS maps. These sources show neighborhoods and properties from a variety of angles inaccessible to the appraiser in the car or on the ground. Some tools include the ability to measure distances, angles and areas. Others combine visual data with invisible network information, such as utilities, or with property data, such as age distributions. Combined, this information can make the virtual realm a more powerful option for the appraiser to analyze a location than a physical site visit. I should also clarify a misconception implied by your question. Property data collection does not involve comparables in any way. It is strictly limited to observing and describing the subject property. The task of analyzing markets, comparables, and value—of drawing conclusions—will remain entirely in the realm of the appraiser, not the property data collector.

WRE: Will an actual person be reviewing the PDC Report and deciding whether to order an appraisal, or will this decision be made by an algorithm?

Fannie Mae: We communicate minimum requirements to lenders through Desktop Underwriter® (DU®). The DU messages are generated through our automated models and logic, but ultimately the lender decides whether to exercise the minimum or exceed it. What this means is the decision is derived from a combination of algorithms generating options and people making decisions about those options. We have established business rules for the DU offerings. If a property data collection report identifies features that suggest a complex property or certain other risk factors that trigger a Data & Appraisal decision—in which case a desktop appraisal informed by the property data package is the minimum requirement. People are involved in creating the rules, testing the rules, and monitoring the model that generates the offers to ensure their reliability. Your question seems focused on the decision mechanism, but I should add that we have aggressive quality control requirements for the property data collection. Lenders are required to have eyes-on quality control like what our Selling Guide requires for loan files and appraisals. In addition, Fannie Mae specialists look at a large sample of the property data files that we receive daily.

WRE: Do you anticipate any licensing for property data collectors, certifications, or background checks? Why or why not?

Fannie Mae: In many cases the property data collector is a licensed appraiser. We are testing other labor pools to see how accurately they collect property data. Whether or not they are licensed depends on the legal requirements for their respective professions. For example, one group we are testing is insurance inspectors. To the best of my knowledge, states do not license insurance inspectors. But, insurance companies have a powerful market incentive to ensure their inspectors are knowledgeable about residential construction. In some ways, their knowledge goes much deeper than the typical appraiser. For Fannie Mae, the skillset is most important. Mechanisms such as background checks, liability insurance, and performance monitoring can substitute for licensing in situations where licensing is not available.

>> Take OREP/Working RE’s Bifurcated Appraisal Survey

About the Author

Isaac Peck is the Editor of Working RE magazine and the Vice President of Marketing and Operations at OREP.org, a leading provider of E&O insurance for appraisers, inspectors and other real estate professionals in 50 states. He received his master’s degree in accounting at San Diego State University. He can be contacted at isaac@orep.org or (888) 347-5273.

CE Online – 7 Hours (AQB Approved)

Identifying and Correcting Persistent Appraisal Failures

Richard Hagar, SRA, is an educator, author and owner of a busy appraisal office in the state of Washington. Hagar now offers his legendary adjustments course for CE credit in over

40 states through OREPEducation.org. The new 7-hour online CE course Identifying and Correcting Persistent Appraisal Failures shows appraisers how to avoid CU’s red flags, minimize callbacks, save time, and earn more! Learn how to improve the quality of your reports and build defensible reports! OREP insureds save on this approved coursework. Sign up today at

www.OREPEducation.org.

Sign Up Now! $119 (7 Hrs)

OREP

Insured’s Price: $99

>Opt-In to Working RE Newsletters

>Shop Appraiser Insurance

>Shop Real Estate Agent

Insurance

Send your story submission/idea to the Editor:

isaac@orep.org

by Dan Forrester

54 years in this business, 25% of that was for litigation. What did I learn in my first cross examination? My response to a question was “you don’t go, you don’t know” Has worked well for 1,000’s of appraisal assignment. One other thing, of all the people and/or entities affected by our work, we seem to forget that the depositor’s and stock holders are most affected by the end result of the lending experience since it is their financial consequences.

-by Cotton Cornell

Fannie Mae does not decide what steps I take to produce credible results. I assume all the risk therefore I deiced what is required to produce credible results. Lets not try to sugar coat this! We are all aware this is 100% a money grab for the lenders and AMC’s. The lender is still charging the borrower upwards or $600 for the appraisal and the AMC’s are paying the inspector $50-$75 and $50-$75 for the appraiser. The AMC and the lenders retain the balance. In the end this will only hurt the consumer, the investor, the tax payer and the appraiser. Nobody wins but the AMC and the lender. I find it funny how appraisers who couldn’t make it in the field ran to hide out at fannie mae and they couldn’t drink enough of that corporate cool aid. I do not believe this Radke is not remotely qualified to make any appraisal decisions! Any appraiser who is doing this type of bifurcation work is doing themselves, our profession and the borrower a serious injustice. Wait till the bond market realizes all the the yields have been falsified and the purchased loans where the collateral analysis was flawed. This will end up disrupting our entire economy again!

-by jaydee

I trust me more than anyone else when it comes to the collecting, analyzing, compiling, and then putting together an appraisal report. They want you to use fragmented sources so they can pay you less. Sources that you’re going to need to verify before you compile a report. Errors? Omissions? YOU’RE responsible!!! This doesn’t save time or money for “ME” the appraiser. So, if you’re going to do this as an appraiser; you’re cutting your own throat and throat of your own profession you worked so hard to acquire. I will not be partaking in this endeavor.

-by Mary Thompson

Luckily, I do mostly personal appraisals, but as Rod Bien said above, I will do the property collection part and not have to worry about valuation any more. I do great sketches and data collection so that will be my choice. AND it will take LONGER not shorter if an Appraiser has to rely on the PDC from another party, because if they are doing their job correctly they still have to drive the comps and if they have ANY questions about the data and you know they will, they have to track down that person and get clarification. This is going to be a disaster! PLUS there is no benefit for the Buyer or the Seller. They both think an actual appraisal is being conducted on the home…NOT!

-by Joshua Walitt

The process being tested does not require the appraiser to drive the comps, as I understand it.

-by Anthony Bamert

The Illinois Dept of Financial Regulation published a statement that anyone in Illinois completing an inspection for a Bi-Fur Appraisal must be licensed as either a home inspector or appraiser. Anyone who performs the Bi-Fur inspection that is not, will be brought up on charges of illegal practice of home inspection by IDFPR.. Further, any AMC who provides an inspection by a non licensed person to an appraiser as part of an assignment will be deemed to have violated the State of Illinois AMC act and will face punishment and possible loss of their AMC license in Illinois… strong stuff

IDFPR Appraisal newsletter Feb, 2019,

link to IDFPR statement: https://www.idfpr.com/Forms/DRE/RENews/IDFPR%20Monthly%20Newsletter%20-%20February%202019.pdf

-by Burt Smith

I read this article and it is riddled with errors and inaccurate statements throughout. I still have yet to have anyone with common sense and logical reasoning support why in the world I would depend on another person to relay pertinent data to me, to develop a reliable and SUPPORTABLE opinion of value. Lenders won’t let an appraiser rely on a satellite image to check the surrounding area of a comparable used, but will allow “John the landscaper” to go take photos and complete an inspection of a home for the appraiser, This whole thing is a complete joke, and I’d love to tell someone that actually mattered why.

In addition, living in an appraisal era of CONSTANT SCRUTINY from lenders and Fannie about every little detail in appraisals and adjustments, it’s mind blowing to me they are ok with paying someone who is not even a Realtor, much less an appraiser to go determine conditions, finishes, and updates. Not even taking into account external obsolescence’s and factors appraisers have spent YEARS determining, analyzing and reporting.

This is nothing more then a way for lenders to try to save a dollar or a day on turn time while putting the same liability on the ignorant and misguided appraiser who chooses to participate in this appraisal form/type.

Here’s an idea, instead of lenders paying “Reasonable fees” that are determined from affected data in the first place, pay a reasonable fee for the time needed to complete and satisfy tons of requirements, tons of miles on a car, and liability that is commensurate with let’s say what a plumber makes these days, not a fee that mirrors what my dad was charging for appraisals in the 1980’s.

Respectfully,

Burt Smith

-Broker-Owner

Caldera Real Estate Group

Certified Residential Appraiser

by Robert E. Curry

I am a retired Certified Residential Appraiser. I worked in the industry for 19 years and retired in 2014. Where can I find out if I am qualified to do the Bifurcated Appraisal

-work.

by Michael Mondello

There is no way that I’m going to cooperate with this. You cannot dumb this process down.

-by Rod Bien ASA IFA

The question was not answered…………who takes the comp photos for the 1004P? Heck, by the time you factor in gathering a list of possible comps (usually 10-15) and drive to the area to obtain their photos for the 1004P, I don’t see the cost savings, because it only takes another 30-60 minutes to measure, observe, photo and analyze the Subject. A large AMC told me that the PDC fee is going to be 45-percent of a full 1004 fee. So if I take the VA’s publicized fee in Oklahoma County of $500, that equates to $225 for the PDC and therefore the 1004P must be $275. Does the $275 for 1004P include driving the comps? What do you want to bet that we (Appraisers) will never see these fees, as they will most likely be much lower. If the PDC fees are $225, I will soon be changing careers from a Licensed Appraiser to a Non-licensed data collector who is not subjected to all the stress as that of an Appraiser, and is not required to carry E&O, MLS fees, License fees, CE, maintain USPAP compliance. Wow, that will save me a monthly expense of about $300 per month, just to be an Appraiser. All I will need is a tablet, tape measure (or laser) and a vehicle. I will do about 3 PDC’s per day ($675) and make much, much more that I can as an Ethical Appraiser. Licensed Appraiser will soon be a thing of the past.

-by Mary Thompson

Amen!

-by Rod Bien, ASA, IFA

Furthermore, it is my opinion that bifurcated, or otherwise chop shop reports are designed for “cookie cutter” properties, but it has been my experience on the 2 or 3 1004P’s which I have tested that the assignments were difficult for some reason or another (new construction, rural, acreage, no nearby similar sales, large high value homes, cut up 2 story homes, etc). And most of the PDC’s that I have had the opportunity to bid on were for similar complex properties, most of which were large 2 story homes where the upper level is within the hip roofline, therefore very difficult if not impossible to accurately measure. Tell me, are these PDC gatherers going to be copying the County Assessor diagram (property sketch)? They won’t know how to accurately measure a difficult floorplan………heck, many Appraiser don’t know how to. BTW: In my capacity as a Forensic Review Appraiser, I am seeing a growing number of Appraisers who are utilizing County Assessor diagrams instead of their own measurements, however they usually include a comment about how the property was personally measured using ANSI Standards. I believe this is how they justify charging or accepting low fees, in hopes that nobody will notice. But guess what, Reviewers and/or State Investigators will most likely uncover this “Misleading” practice………and unless the Appraiser clearly states that he/she used the Assessor measurements instead of their own, and explains why they did not measure the property, they could end up receiving a failing grade and perhaps in front of a Panel of their peers.

-by Joe Chambers

Who is bifurcating benefitting?

-It’s all about Fannie and their big data file.

There is a distinct lack of mention/focus regarding the consumer/borrower and the costs, timeframe and most importantly, their protection.

“Pay no attention to the man (entity in receivership) behind the curtain”

by Brad Bassi

I really don’t care what you call it. But if you want my signature, my E&O and me to be held responsible then I won’t be doing that for $75, $85 or $100 and tell me I can make it up in volume. This all about money (how little will the appraiser work for) and nothing else.

-by Candy

Amen! You are STILL RESPONSIBLE for an accurate value conclusion. What the 3rd party misses the railroad tracks one street over? Therefore, you missed a location adjustment. Doctors don’t go into surgery blind. They read the patients x-rays or test results. Shouldn’t you look at what you’re signing your value to.

-