|

“One of the best courses that I have had in 17 years!” -Amy H.

|

Editor’s Note: The current edition of Working RE is in the mail. OREP E&O insureds enjoy it free!

Desktop Appraisals: Risk and Reward

By Scott Cullen, Solomon Adjustment Calculators

Many appraisers realize that they can earn more money per hour, with lower expenses, doing desktop appraisals for valuation companies who specialize in that type of work. These desktop clients have convinced lenders that a share of their valuation needs can be met very well with their particular brand of desktop appraisal.

Appraisers who do these assignments spend less time driving and inspecting. After all, the appraiser’s highest and best use is to analyze data and apply that expertise to the development of an opinion of value. As a result, the scope of work for many assignments has changed so that appraisers are paid a relatively high hourly rate for analysis, without paying that same rate for driving their cars.

Whether the scope of work includes inspecting the subject and driving comps, or doing everything from their desk, the appraiser is responsible for maintaining a workfile on each assignment including documentation of their use of recognized methods for developing credible assignment results. This includes support for adjustments.

This is much different from an open house where a dozen agents show up for snacks and a tour of the latest listing in their market area. The reason they are at the tour is to preview the house and provide their expert opinion on the listing price. No methods, no documentation, just an eyeball test. The eyeball test and market experience do not pass muster with the folks who regulate appraisers. Appraisers need facts and analysis.

According to the USPAP Record Keeping Rule, “An appraiser must prepare a workfile for each appraisal or appraisal review assignment. A workfile must be in existence prior to issuance of any report or other communication of assignment results.”

The workfile must include a copy of the report. According to USPAP, it must also include, “all other data, information and documentation necessary to support the appraiser’s opinions and conclusions and to show compliance with USPAP, or references to the location(s) of such other data, information and documentation.”

“A workfile in support of a Restricted Appraisal Report must be sufficient for the appraiser to produce an Appraisal Report.”

“The workfile must be made available by the appraiser when required by a state appraiser regulatory agency or due process of law.”

“An appraiser who willfully or knowingly fails to comply with the obligations of this RECORD KEEPING RULE is in violation of the ETHICS RULE.”

How can a desktop assignment that pays under $100 possibly be profitable, given the responsibility to comply with USPAP by developing market supported adjustments to the comparable properties? In my experience, the only way is to use depreciated replacement cost to adjust for GLA, Bath Count, Garage Count, Basement Size and Basement Finish. It will take some time to set up a worksheet, but once you have done that, the calculations can be done in less than one minute per report. If you can develop market-based adjustments for five or six property characteristics in less than one minute, you can make money doing desktop appraisal assignments.

(story continues below)

(story continues)

Power of Depreciation

You may be wondering what cost data has to do with a desktop appraisal that does not include the cost approach to value. That is a great question. The answer is that cost data is the basis for knowing depreciation. When depreciation is known, we know two things. First the obvious: we know the part of cost for which the market pays nothing. More importantly, we know the percentage of cost for which the market does pay. Stated in appraisal terms, we know the contributory value of the improvements. Speaking in the vernacular, we know the cents on the dollar that have been paid for a house.

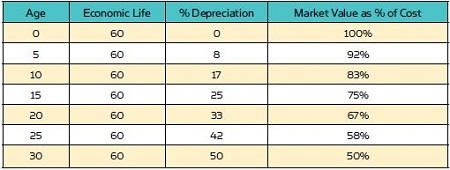

Figure 1: Depreciation percentage for Q4 houses of different ages

Assume you have identified the best comp available for the house you are appraising, and it sold for $200,000. If the land is worth $50,000, the market has shown that the contributory value of the improvements is $150,000. If that house has a replacement cost of $250,000, we could say that the market paid 60% of cost for the improvements ($150,000 / $250,000) and that there is 40% depreciation ($100,000 / $250,000).

Because it is the best comp available, you have a good idea that the subject property, being in equal condition, quality and site value, has also depreciated 40% and the market would pay 60% of replacement cost for the improvements. If a second garage stall costs $10,000 and the market is paying 60% of cost, a market supported adjustment for the second garage stall is $6,000. Likewise, if a second bath costs $9,000, a market supported adjustment for a second bath is $5,400.

How do you know the percentage of depreciation? Part of the answer is

scope of work. The appraiser never sees the exterior and nobody sees the interior of the subject property. Usually, the scope of work states that the appraiser is to assume that condition is average. The second part of the answer is to be able to judge the quality of the house, and know the economic life for that quality rating. If the house is a Q4, and your cost data states that economic life of a Q4 is 60 years, you have one half of the depreciation calculation. The other half of the equation is Effective Age. If the house is assumed to be in average condition (scope of work) and chronological age is 30 years or less, then depreciation is most likely to be the chronological age divided by the economic life.

How do you support an estimate of Effective Age if the chronological age is over 30 years? With the assumption that the house is in average condition, Effective Age is less than chronological age in older houses. Estimate Effective Age the same way you would if the assignment is for a traditional appraisal on the Uniform Residential Appraisal Report.

The cost data I use states that economic life for a Q3 is 70 years. Depreciation calculations will therefore be different for a Q3. For example, a Q3 that is 30 years old has 30/70 = 43 percent depreciation vs a Q4 that would have 50 percent depreciation at age 30. Within the scope of work of a desktop appraisal, that is all we need to know about depreciation. This brings us halfway to a good understanding of depreciated cost. The other half is cost.

Cost Data

Residential cost data is available from several providers. They have two things in common. First is that they are based on survey data. Like any survey data, the results tend to form a bell curve when plotted. Two builders are not going to agree on the cost of the same house, but with an adequate survey size, the cost data that is available to the appraiser is a valuable point of reference. If the cost data is “too low,” depreciation will be low and depreciated cost will be similar to “high” data with higher depreciation. Either will work for you in developing adjustments, so stick with the data you can use as an unbiased, third party, credible source.

Go to your trusted cost data and develop cost figures for features such as a second garage stall, second bath, fireplace, etc. Remember that costs for a lower quality rating will be lower than for a higher quality rating. Economic life is likely to be different at some quality ratings, so be careful with your depreciation calculations.

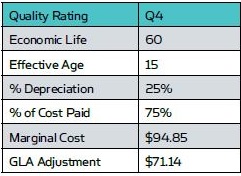

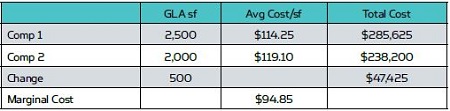

To handle features such as GLA, you need to use your cost data to drill down to marginal cost. For example, 2,000 square feet of GLA may have an average cost of $119.10 while 2,500 square feet of GLA may be $114.25. To get marginal cost (the cost of one more square foot of GLA), subtract total cost of 2,000 square feet from the cost of 2,500 square feet. Divide this dollar amount by the difference in square feet to get the marginal cost of GLA, which is the GLA adjustment for a new house (See Figure 2).

Figure 2: GLA Adjustment

Then use your estimate of Effective Age to calculate the percentage of depreciation. Use the percentage of depreciation to get the percentage of cost being paid in the market. Multiply the cost of GLA by the percentage of cost being paid in the market to get your market based GLA adjustment (See Figure 3).

Figure 3: Market-based GLA Adjustments

USPAP requires appraisers to use a recognized method to develop and support adjustments for desktop appraisal assignments. Depreciated replacement cost is a recognized method for developing and supporting adjustments. The depreciation half of the calculation is inferred by the scope of work of the assignment. The replacement cost piece can be developed periodically from credible, unbiased third-party cost data providers.

If you are handy with spreadsheets, you can build a depreciated cost workbook on your own and produce USPAP compliant desktop appraisals with instant support for your adjustments. If you are not so inclined, there is software designed to do the calculations, and provide the cost data.

“I have recently completed the best appraisal class of my 30 year career (How to Support and Prove Your Adjustments through OREP.) ” -Susan D.

Continuing Education: How To Support and Prove Your Adjustments

Presented by: Richard Hagar, SRA (7 Hrs. Online CE)

“One of the best courses that I have had in 17 years!” -Amy H.

Must-know business practices for all appraisers working today. Ensure proper support for your adjustments. Making defensible adjustments is the first step in becoming a “Tier One” appraiser, who earns more, enjoys the best assignments and suffers fewer snags and callbacks. Up your game, avoid time-consuming callbacks and earn approved CE today!

Sign Up Now! $119 (7 Hrs)

OREP Insured’s Price: $99

About the Author

Scott Cullen is a Certified Residential Appraiser from Eagan MN who is a partner in the development of the Solomon Adjustment Calculators. You can try it on a free 14-day trial at www.solomonappraisal.com.

Send your story submission/idea to the Editor: isaac@orep.org

by Mark Mason

I’m all about it! Let me do desktops from an island for $50 a pop.

-by Mike Ford, AGA, GAA, RAA, Realtor(r)

So much assumptive information that the credibility of the argument ‘for’ desktops being valid is undermined. That a ‘cost service’ estimate of my subject’s total economic life OR its accrued depreciation from all causes can be an accurate market perception is pure speculation. Sixty years? Really? Why not 100? Or, why not 40 for an average quality brick building as used to be taught in both real estate and appraisal courses? It is extremely unlikely that an average quality SFR really does have a 60 year economic life expectancy. How many 1958 year built houses can we find that have had no major or significant updating in the last 60 years? Plumbing, heating, electrical, roofing and kitchen all original and commanding top dollar in the marketplace still? Truth is that most houses require updating after about 30+- years, or a penalty is perceived in the market. Many may need it after 1/2 that time.

The real issue here is not support for depreciation estimates (which are ALL ASSUMED in a desktop anyway). The real issue is whether such analyses or “appraisals” have any right to be labeled “appraisals” in the first place without some type of limitation disclosure beyond ambiguous, carefully parsed scope statements that are designed to mislead should not be permitted to replace identification as some form of extremely abbreviated value analysis that falls far short of any traditional appraisal. TAF has changed definitions yet again to accommodate diminished appraisal quality and reliabiity.

David Rij pointed out better quality desktops may well take 2 to 3 hours to perform. I agree. Im not likely to dismiss a desktop out of hand that I know included several hours of honest appraisal work by an appraiser that knows without being told, that this is important.

Conversely, I dismiss ALL advertised and posted $25 to $100 an hour third party inspected garbage products that I have seen to date. NOT ONE allows adequate time for USPAP compliance. Without fail, every one observed so far in either template or actual copy has fallen short of USPAP though each claims compliance.

Whats truly amazing to me is that E&O carriers have not come out in opposition to these spurious products, or at least have not published much stronger cautions about their preparation.

-by Henry T. Casado, MAI, SRA, AI-GRS, AI-RRS

What is the support for 60 years economic life?

-by David Rij

Who says a desktop appraisal has to be $100 or less and why does it have to be done in 5 minutes? I’m exaggerating on the time, but there are better quality desktops that start at $200 and are completed in 2-3 hours rather than 30 minutes. The most important part of the appraisal process is the final value estimate and in my opinion that’s worth at least half of a full appraisal fee.

-