|

>> See Past News Editions >> Click to Print Protect your license and your livelihood with the Expert’s Guide by Tim Andersen, MAI. Click now 2015 AMC Guide |

First Enforcement of C&R Fee Provision: Louisiana Makes History

by Isaac Peck, Editor

Nearly five years after Dodd-Frank set forth rules regarding Customary & Reasonable fees (C&R) for appraisers, an agreement last week between a state board and an Appraisal Management Company (AMC) is the first evidence of enforcement. The bottom line for appraisers is that they may be finally on their way back to customary and reasonable fees.

On June 4, 2015, the Louisiana Real Estate Appraisers Board (LREAB) issued a Stipulations and Order Memorandum (SOM) wherein Coester Appraisal Management Group, also known as Coester VMS, offers no admission of guilt but agrees to follow the current Louisiana fee schedule for a period of 12 months and pay $5,000 in administrative costs. Coester also will submit Quarterly reports to the Board for a period of 12 months, which list “all appraisal orders in Louisiana, the fee paid and the date payment was made to the appraiser.”

In the Final Order obtained by WRE under the Freedom of Information Act, Coester agrees not to contest the case while simultaneously alleging that, “it (Coester) complied with the federal law, and as such, it was in compliance with Louisiana Law.” In contrast, the Louisiana Board alleges that “Coester Appraisal Management Group did not use established fees set by an objective third party or use the factors set forth” in Louisiana law, in determining fees paid to appraisers.

LREAC and the Appraisal Institute

In a press release published by the Louisiana Real Estate Appraisers Coalition (LREAC), Joseph Mier, SRA, AI-RRS, RAA and President of LREAC stated: “This is an important recognition that the Louisiana Appraisal Board is addressing complaints made by appraisers in reference to C&R Fee rules being followed. This is a step in the right direction for transparency for consumers and for the health of the appraisal industry going forward. Working together with Louisiana appraisers, the Louisiana Chapter of the Appraisal Institute and the national Appraisal Institute, we hope that this will help to advance transparency for the appraisal industry in the future. Appraisers are reminded to report any violations of the current AMC laws and rules to the LREAB so that the law is adhered to fairly across the board for everyone.”

(story continues below)

(story continues)

In an interview with Working RE, Mier stressed that it’s important for appraisers to not adopt an “us versus them” mentality with regards to AMCs. “The goal for appraisers should not be to harm AMCs. The real message is that we need to work together,” Mier said. “AMCs have a purpose, but the business model of some AMCs have hurt the entire industry. A business model that takes a significant portion of appraisers’ fees and pays non-C&R fees, as per the Dodd/Frank Rules, results in high quality appraisers leaving the industry or refusing to work for AMCs altogether. It also discourages young professionals from joining the industry, which is an important consideration given that the latest Appraiser Quality Monitoring requirements have made it even more difficult to be an appraiser. Both appraisers and AMCs have an interest in compensating appraisers fairly with a minimum C&R fee,” says Mier.

Finally, Mier says that LREAC is appreciative of the Louisiana Real Estate Appraisers Board (LREAB) for their efforts to follow up on real complaints by appraisers and for the changes that Coester VMS is making. “We appreciate Coester VMS recognizing the need to follow one of the two presumptions of compliance by utilizing the current fee schedule that’s been established by the third party fee survey in Louisiana. They have agreed to make several important changes and we appreciate that. These industry issues can be repaired but the current business model must change going forward. It will take all industry partners to be involved to make that happen.” says Mier.

North Carolina

This is not the first time that Coester VMS has been a target for state boards. Besides being investigated by LREAB, Coester was also sanctioned by the North Carolina Appraisers Board for failure to pay appraisers on time. In a Consent Order signed October 13, 2014, Coester admitted that it failed to pay appraiser invoices on time. As a result of the Board’s investigation, it was discovered that 1,066 payments to appraisers were made beyond the 30 day requirement mandated by North Carolina law. Consequently, Coester was ordered to pay a civil penalty of $10,000 and had its AMC license suspended for a period of six months. However, the suspension was stayed until February 2015.

(story continues below)

(story continues)

What are C&R Fees?

In Louisiana, AMCs may comply with the C&R Fee Legislation by using “objective third-party information such as government agency fee schedules, academic studies, and independent private sector surveys” to develop a fee schedule. However, the Louisiana law, modeled after Dodd-Frank, also specifies that “fee studies shall exclude assignments ordered by appraisal management companies.” If an AMC decides not to use a set fee schedule based on independent fee surveys, the AMC “shall maintain written documentation that describes or substantiates all methods, factors, variations, and differences used to determine the customary and reasonable fee for appraisal services,” which, at a minimum, includes six elements an AMC must document and analyze for every assignment order.

In its complaint against Coester VMS, LREAB alleges that Coester was using neither established fees set by an objective third party nor the factors set forth in Louisiana law. To read the Louisiana law in its entirety, click here: http://www.reab.state.la.us/AMC_Rules.html.

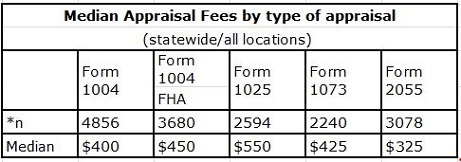

When Louisiana’s law first passed in 2013, LREAB commissioned a statewide survey to be conducted by the Southeastern Louisiana University Business Research Center (SLUBRC). Because Dodd-Frank specifically excludes AMC-ordered appraisals in determining C&R fees, the survey focused on fees paid by banks, not AMCs. The survey also includes appraiser input for comparison, based on their work with banks and other non-AMC clients.

The table below represents the median appraisal fee reported in the survey paid by banks directly to appraisers. (Read the complete fee survey report here).

Looking Forward

This first enforcement of C&R fee provisions is a victory appraisers have long waited for, according to Richard Hagar, SRA. Hagar says it’s likely that Louisiana’s example will embolden other state boards to take action on C&R fees. “Louisiana is one of the first states to take action like this, and there will be more coming from other boards. More and more states will begin looking at the issue of C&R fees, talking about the process involved in enforcing them, and starting to do something about it,” says Hagar.

The Dodd-Frank Act and other federal regulations have granted the authority to license and regulate AMCs to all states, and according to Hagar, that includes enforcing C&R fee provisions. Hagar also makes a nuanced point regarding C&R requirements: “To date, currently 35 states have enacted AMC licensing laws. More will follow. As they enact those licensing laws, the states will have the authority to enforce C&R fees. States don’t necessarily need to write C&R enforcement powers into their AMC regulations the way Louisiana did. It’s in federal law. Once it’s in federal law, AMCs must operate under federal guidelines and their state boards have the authority to sanction them for violating those laws,” argues Hagar.

Increased regulation and enforcement of AMCs will help the industry, argues Hagar. “In order to stick around, AMCs are going to need to be more business-like and operate more ethically. As enforcement of C&R fee provisions finally catches on, we should see a decrease in lowball appraisal (email) order systems, because shopping for the fastest and the cheapest appraiser is prohibited. Appraisers, in turn, should be freed to raise their fees and provide a superior product,” says Hagar.

Upcoming Live Webinars:

Thursday: How to Support and Prove Your Adjustments – A Closer Look

Presented by Richard Hagar, SRA

Part 1: Available Now

Part 2: June 11th, 10 – 12:00 p.m. PST

“I have been an appraiser for over 20 years and have rarely heard the information that Hagar was teaching from anyone except my mentor and former boss who is an MAI. Hagar’s class is not only essential, it is exceptional. He manages to keep it interesting as well as highly informative. I will remember his name for future continuing education classes. Thanks for sponsoring such a high quality instructor. – John P Thermos

Updated and expanded, Hagar shows you how to properly support your adjustments- the foundation of good appraising! Regulations state that appraisal adjustments cannot be based upon an appraiser’s opinion. Failure to provide proper proof and analysis to support your adjustments means a rough road ahead: state board complaints, panel removal, lawsuits, even license revocation. Fannie Mae cites “the use of adjustments that do not reflect market reaction” as the number one reason an appraiser can be “blacklisted.” This training is critical in helping appraisers avoid catastrophic appraisal failures. Sign Up Now!

Back by Popular Demand!

This webinar will help you utilize quick and simple methods for proving adjustments that improve the quality of your reports and help you avoid problems, blacklisting and legal actions. Sign Up Now!

Save with a Season Ticket!

Enjoy the entire summer webinar series at your leisure (live and recorded) and save: June, July, and August Webinars (six webinars) for a single price!

Regular Price: $237 Summer Series Season Ticket: $149

Summer Series:

June- How to Support and Prove Your Adjustments

July-

Part 1: How to Get What You’re Worth (Working with AMCs)

Part 2: How to Work Profitably With AMCs

August-

Part 1: Running an Effective Appraisal Business

Part 2: Efficiency Through Technology: Mobile Tools and Paperless Appraising

Enjoy the Entire Series! Save $88 with a Season Ticket!

About the Author

Isaac Peck is the Editor of Working RE magazine and the Director of Marketing at OREP.org, a leading provider of E&O insurance for appraisers, inspectors and other real estate professionals in 49 states. He received his Master’s Degree in Accounting at San Diego State University. He can be contacted at Isaac@orep.org or (888) 347-5273.

>Click to Print

>New: Collateral Underwriter Blog: Find answers, offer solutions.

>Opt-In to Working RE Newsletters

Send your story submission/idea to the Editor: dbrauner@orep.org

by Mike Ford CA AG; SCREA, AGA, GAA, RAA

When median fees are used it only means that exactly half of them are less and half of them are more. How does THAT equate to either customary or more importantly “reasonable?”

Try this instead. You may have to deduct 10% for effect of local area multiplier.

-http://mfford.com/html/c___r_fees.htm

by Ryan Brennan

I took a few orders from Coester last year. The fees were c&r but it occasionally took a while to get paid. They even paid me twice for the same assignment. I actually have integrity (look that word up if you’ve never heard it) and emailed the accounting department at Coester to get it all straightened out. I stopped taking their orders because they are super disorganized and no one that works there seems to know what they’re doing, but about 8 months ago they mysteriously tried to withdraw $400 from my account. (We went on direct deposit after they double paid me and I gave them my account and routing numbers.) I emailed their accounting department and asked why they were attempting to debit my account which was surprising since we hadn’t done business in months. Their accounting person asked for more details; I screen shotted my bank account website. No one ever got back to me. I called my bank and asked that they be blocked from my account and have not accepted an order from them since. They are so stupid and keep soliciting orders but I don’t accept and keep asking to be removed from the roster. I’m curious if other appraisers had their accounts debited; if I hadn’t been paying attention they could have easily stolen my money. I still have the screen shots, emails, etc. horrible company. If you have any self worth at all you will stop taking orders from them. It’s only a matter of time until these incompetent people turn on you.

-by Mike Ford

I just received word yesterday that an old colleague is till doing work for whatever company LSI morphed into. I jokingly asked if they are still paying $175 gross fee to appraiser? I was told “No. It is less AND they have to pay an upload or processing fee out of that!” Amount reported? $165.

I don’t care WHERE you are in America today. THAT is neither customary NOR reasonable and the company damn well knows it. They should have a class action suit against them big enough to shut them down for good. They’ve (They being LSI or who they changed into) been low balling appraisal fees since 1993.

Lets see. $165, minus $10 gouge to upload = $155. Less minimum of 25% home office overhead = $116.25. Divide by 8hrs for a 100% USPAP compliant UAD report with properly analyzed 1004MC = $14.53.

That’s $0.47 a hour LESS than many want McDonalds and other fast food workers to get! At least at MickeyDs you get fed and don’t have to risk getting sued.

-by Robert Lawrence, retired

Yes but herein you get to sign your name and hand out a business card! Oh, go to classes too? darn.

-by Mike Ford, CA AG, SCREA, AGA, GAA, RAA

Martin, Your observation is he obvious one, but lets not downplay the good work that LREAC did. I guarantee this company took more than a $5k hit in bad PR. Even if it IS profitable (so far) to scam the game-sooner or later it will all catch up with them.

-by Jeremy Hall Appraisals - Colorado

Audit all of them, to see who’s in compliance, and who is not. How unfair to only fine one company in one location, when it’s common knowledge that such activity is most certainly not limited to just that one company, in just that one location. I’ve got the emails to prove it, and so do 50,000 other appraisers.

-by Robert Lawrence, retired

Among the several reasons I decided to “flee the fee” was when clients were dictating my business practices. I refused and lost business. In the end I would not play the game at their rules (too many of them with the worst getting a large share of their market) so I iced my lice. Four decades was long enough anyway. For now, those of you still carrying the flag, fight on and take the hill back! It is yours and your highest and best use (+$) should not be dictated by the false market. Best of luck and take good care.

-by Robert Lawrence, retired

here here. fight now and fight right since you are!

-by Michael F. Ford, CA AG, SCREA, AGA, GAA, RAA

Louisiana took a giant step in the right direction but before anyone else jumps on that states fee schedule as being the metric; lets recognize the costs of working and living in that state are different than those in 49 others plus DC, and territories.

The federal government uses percentile multipliers based on long term studies of COLA differences. So in California (127%), a similar MEDIAN fee might well be $508.00 for the same NON COMPLEX, conforming loan limit appraisal work. I still think that is too low for a non home-business where rent, utilities and separate phone services are required; not to mention office staff to respond to client needs when the appraiser(s) are out in the field. Clearly more work is needed on what is “reasonable”.

When other states do their fee studies, they also need to make an adjustment for the influence low AMC fees have had on the overall competitive appraiser “market”. Its no different than what we do when we realize that fully 50% to 75% of all activity in a given market is REO sales or resales. We KNOW (and data typically supports) that current pricing IS affected by the lower, distress sales associated with the foreclosures. When foreclosures disappear; inventory is down, and effective demand is adequate, then prices go up.

Appraiser fees are no different. When AMCs low fees are no longer a factor; after the industry has lost 1/3 of its practitioners, and MORE work is required than in any time past then fees MUST go up under any competitive scenario for professional work!

Louisiana made a start. The rest of us need to pick up where they left off and INSIST on REASONABLE FEES.

-by Robert Lawrence, retired

Since I still have an axe that is not ground down yet, I have read many of these and you good folks are same-paging with good intent. Now the process needs to trickle down to the majority who are buying this rotten half-eaten apple. Yes, most of you are “independent” appraisers who cannot fix fees or much less openly discuss them I suppose, but it is really time to communicate to the highest level possible, even to your “competitors”. The only real competitor for a small business is yourself, since you run the game, call the shots and make your own bed. The more of us/you that hit the sack well, the better as a profession we can sleep. If you are a true professional, then you should have sweet dreams. Do them well first and foremost and you should find compensation accordingly. aloha

-by Martin Randolph

Did I read it correctly? the fine was $5,000? That’s not enough to put gas in the corporate jet for a quick $2,500 lunch in Aspen. I think I would continue to low ball fees and basically rob hard working appraisers blind. What a farce! If they underpaid $100 on 10,000 appraisals that’s a million dollars or .0050 %. Incredible! I would like to know how many appraisals went through the company and how much the average fee paid compared to the reasonable and customary fee.

-by Jeff Weks

The solution to these and many other issues with AMC’s is for all appraisers to stand up and not give in to low ball fees to begin with. As well as ridiculous updating and scheduling requirements. Coester is also in court in Virginia fighting to stay on the Virginia Real Estate board for violations in that state. Its obvious this is one AMC none of us should be working for.

-by Robert Lawrence, retired

Your calculator is sharp. so true. bad deal.

And as to working for the crooks, my old staff and co-appraisers (some of them) feel they have no other choice. I believe they are right and it is sad but true. The spring will jump back but will it be too late for the bed that has been made?

-